Benchmark Capital

Why Benchmark Capital invested in eBay, Uber, and Riot Games

There are a few companies that define a decade of startup investing. In the 1990s, it was eBay. In the 2010s, it was Uber. While these seem like completely different business models today, they rely on a similar theme around network effects that is at the core of the investment thesis of the VC firm we’re going to talk about today: Benchmark.

Brief History:

Benchmark was founded in 1995 at a time when venture capital was dominated by headline firms like Kleiner Perkins, Sequoia Capital, and Accel. However, these firms had their soft spots, and Benchmark was poised to take advantage of them. For example, Kleiner Perkins was synonymous with John Doerr. Yes, Vinod Khosla was there at the time and was widely respected, but John Doerr was viewed as the top investor in the valley, and everyone wanted him on their board. If you took money from Kleiner you were happy to have that stamp of approval on your company, but if you couldn’t get John on your board, there was a sense of disappointment because John was not going to support your company if he was not on your board.

Benchmark uniquely positioned itself as the first venture capital firm to give equal economics to the small number of partners within the firm. Rather than the partner who led the deal taking most of the carry on that investment, the five founding Benchmark partners were each given an equal 20% of the carry on their fund regardless of who led what deal for what company. The result was a partnership that pursued and won deals as a team and provided the company with the most fitting board member from Benchmark regardless of who led the deal. No partner had an unequal focus on certain companies in their portfolio depending on whether they led the deal or not. Benchmark was creating a firm that truly incentivized the firm’s success with their company's success.

As a result, Benchmark has solidified itself as one of the greatest and most consistent venture capital firms of the last 30 years, defined by its seventh fund, which returned somewhere around 20-25x to its LPs, and its first fund, which returned at least 50x to LPs, potentially even 92x, making it most likely the greatest returning venture multiple of its size and scale.

Today, we’re going to talk about why Benchmark invested in decade-defining companies like eBay and Uber and another notable win that has many lessons to learn from in Riot Games. As our traditional format follows, we’re going to investigate why Benchmark invested in these companies, what their general investment theses are, what they look for in founders, how you as a founder can position yourself to raise capital from Benchmark, and lastly, we will take a look at some HUGE misses they’ve had throughout their near immaculate journey. Hint: We talked about some of these companies in last week’s Sequoia essay.

Here we go.

Why did Benchmark Invest in eBay?

Remember in the Sequoia essay where we discussed the long-held maxim that wins lead to more wins in venture capital? Well, eBay was one of Benchmark’s first investments, and boy, did they set themselves up for more wins early on.

eBay is interesting because, in hindsight, it is an obvious venture investment, but at the inception of the internet, it was a very non-consensus one. In fact, Benchmark was the only venture capital firm to give the eBay team a term sheet. The only other option on the table was to sell eBay to a newspaper company for $50m, which the founder, Pierre Omidyar, wisely turned down.

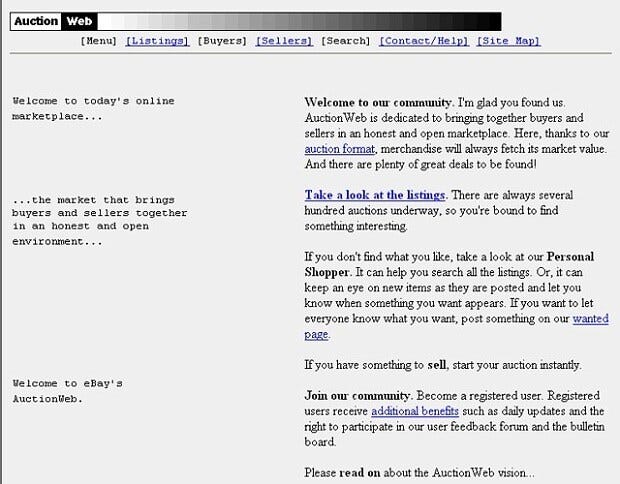

So why was something seemingly so obvious so non-consensus? Well, the early days of eBay were very crude. For example, here is their website in 1997, the year Benchmark invested (with its former name - AuctionWeb):

So yeah, crude.

But what former Benchmark partner Bob Kagle found when he began using the product, as many eBay users discovered, he could find things he couldn’t find anywhere else that pertained to his hobby. In this case, one of the most niche hobbies I’ve ever heard of, but Kagle was a collector of hand-carved fishing lures, and as anyone reading this could assume, it was pretty hard to find a place to purchase such a product.

Kagle found a seller based in his hometown in Michigan that sold hand-carved fishing lures. While Kagle lost the bid on the lure, he felt the powerful unlock of being able to buy anything you wanted from the web. In 1997, this was revolutionary, especially for niche products. I doubt it was even possible to get a hard-carved fishing lure in the Mountain View town where Benchmark was based. Kagle would’ve had to find a business that sold products like this, likely in a Yellow Pages because I’m 99.9% sure any business selling hand-carved fishing lures did not have a website in 1997. He would’ve had to get his map, and figure out how to drive to this obscure business likely far from his home address.

Instead, all he had to do was go online, click the link to hand-carved fishing lures, pick out whichever one he liked most, place a bid, and see it at his door in a week or two. What an insane unlock!

Kagle recognized this unlock, but many other investors didn’t because how many people would want hand-carved fishing lures? Or how many people would want beanie babies, a common product bought and sold on eBay, or how many people would want BROKEN LASER POINTERS, because, the first product ever sold on eBay was a broken laser pointer for $14.83! The founder, Pierre, even messaged the buyer to say, “Are you sure you want this? It’s broken.” The buyer unbelievably replied, “I’m a collector of broken laser pointers.” The point is that anything could be bought on eBay from anywhere around the world. The concern that most investors had, however, was that most transactions were odd niche ones like these. Could that really scale?

Benchmark’s non-consensus view that eBay could build a billion-dollar-business off of this niche marketplace is supported by a quote from former Benchmark partner Matt Cohler. While this is stated post-investment, I’d assume this quote was in the DNA of Benchmark at the time of this investment. Cohler said,

“I think the real litmus test is if you believe that either today or in short order there's a path for both the buyers and the sellers to look at this place as the preferred place where they accomplish this transaction then you've got something really really interesting…

Very early on we were lucky to be the series A investors at eBay… and early on they built a business on the back of this fish tackle collectable vertical…

Early on if you were nerding out on fishing stuff like duck decoys and fish tackle collectibles, it pretty early and quickly became this is the place where you go to get that stuff, and that was obvious and organic and not forced and maybe it was limited but that was something really interesting and alive and I think that same thing applies to a lot of the marketplace businesses that we've invested in.”

What I love about this quote is the last sentence where he says this is the place you go to get that stuff, creating a living marketplace. Rather than eBay becoming a place to get books or clothes or another generic item you could get anywhere, it became the place to get this highly specific item.

Why this is prone to scale is because it builds that reputation as the place to go for differentiated items, so while at first, it’s fishing lures and beanie babies, it’ll soon become trading cards and rare shoes and other unique items that millions of people are eventually looking to buy. They’re going to the place with the reputation of this is where you get unique things.

eBay is a genius product, but an even more genius roll-out plan of targeting and honing in on each individual market as they begin to pop up on the site, and cultivating them to host themselves on eBay as the preferred buying and selling destination.

Why this is sustainable can be defended by this quote by current Benchmark partner Sarah Tavel, describing how an increase in customer happiness leads to a decrease in customer retention. She says,

“GMV (Gross Merchandise Value) is not to say that it's not a useful measure, but it's not a thing you want to drive towards. If you're just driving towards maximizing GMV, you're going to end up with scenarios where you're getting big numbers but you're not actually creating any enduring value.

Instead what you want to do is focus on creating what I think of as happiness. Happiness to me is something that incorporates the holistic experience that you create for your buyers and your sellers. It's almost the delta in a way the value you create and the value you capture from your marketplace.

People talk about minimum viable product. What I think for marketplaces, I call that minimum viable happiness… How do you measure happiness? It must be frustrating for engineers to hear that's the optimization function.

What I ended up coming down to is retention. My friend, Casey Winters, who I work with at Pinterest and is now the Chief Product Officer at Eventbrite—just a great marketplace thinker—said something when I was talking to him about happiness. He told his team that product/market fit isn't when your user stops complaining. It's when they stop leaving.”

Once again, this quote defines eBay’s strategy. They weren’t trying to be Macy’s.com and just sell any products to maximize revenue; they were building a marketplace around satisfying a user’s desire for that intensely unique product that he or she could not get anywhere else.

As a result, eBay was building both a marketplace and a community because buyers and sellers were now meeting people with the same bizarre interests as them. I’m sure there have been many instances where someone bought a unique item from a seller that spurred a conversation about their collectable hobbies, which spurred some type of relationship. You could argue that eBay is both a niche marketplace and a niche social network in that regard. I’d be really interested to see some type of data on how many friendships were made on eBay due to an incredibly unique transaction.

For example, if I’m someone in Washington D.C. who collects rare Yu-Gi-Oh cards, which may or may not be true, I can get connected with some seller in Mobile, Alabama who also loves rare Yu-Gi-Oh cards. We can talk about what cards we have, what cards we want, why he or she is selling, and spur a conversation on a topic I may or may not be scared to talk to my friends about.

Like Tavel said in the quote above, people were ecstatic they found a place where they could satisfy their unique hobbies physically through the products and mentally through the relationships that may have been created through these transactions. They were extremely happy customers, and they would never leave the product.

And if your product has no churn, you can only grow.

In 1990s venture capital, dominated by white men and their business or engineering degrees, the word community was laughed at anytime it came up during a pitch. But the Benchmark partners who heard Pierre Omidyar’s pitch remember how frequently he used the word community and that the users of eBay felt they were truly part of this unique community.

So, while many VCs at the time dismissed this idea of serving a niche community and building that community and driving the happiness of that community, Bob Kagle, who had experience in the retail sector, knew how important treating customers like a community was. He knew it was a differentiated way to drive customers to your product and retain them for as long as they felt a part of that community.

This is all great, but what about the actual numbers of the business? After all, communities and happy customers are great, but this business has to make $100m+ in revenue for it to be a venture-backable company.

Well, they had good numbers. By the end of 1996, a few months before Benchmark invested, eBay had $400,000 in monthly revenue with a 40% monthly growth rate! Even crazier, half of that revenue was going straight to the bottom line as profit! UNBELIEVABLE.

So yes, they had good numbers.

As a result, Benchmark invested $6.7m in eBay for 22.1% of the company. eBay would never touch the money. Pierre didn’t need Bob Kagle and Benchmark’s money; all he wanted was their counsel and connections. A key reminder that VCs can’t just seek out great investments; they have to be worth their price. For Pierre, Benchmark was worth 22.1% of eBay.

What followed is one of the greatest returns in venture capital history. eBay’s exponential growth continued, allowing them to go public just one year later in 1998. Benchmark held their stake valued at around $150,000,000 at the IPO up the tech bubble before beginning to distribute shares in April of 1999 when their stake was worth $5,100,000,000!! (nearly $10b in today’s money)

It is unknown exactly how much Benchmark made on their investment since eBay’s stock would begin to fall dramatically a year later, but if we look at the math on a $6,700,000 investment that generated $5,100,000,000 in value just two years later. You’re looking at a 761x and a 2,659% IRR! Again, I don’t know enough to confirm this is the greatest investment ever, but I would be willing to bet it is.

Being non-consensus and right sure has its perks.

Why did Benchmark Invest in Uber?

So let’s jump ahead about a decade to Benchmark’s next company and industry-defining investment in Uber.

Interestingly, the early 2000s were kind of a lull period for Benchmark. There weren’t a lot of investments after Fund One, which included eBay, that led to strong exits. Investments like OpenTable and Zillow were great exits for Benchmark in 2011(more info at allthingsvc.blog, but there weren’t too many other notable exits between 2002 and 2011.

Good thing Benchmark had another “one of the best investments of all time” up their sleeves.

As I mentioned, Benchmark just witnessed a big win with OpenTable. They roughly 30x'd that investment and were really starting to see the power of network effects. By now, they had witnessed it with eBay and had seen it with OpenTable, and former Benchmark partner Bill Gurley was starting to think about what other industries were prone to network effects. Gurley said,

“Having come out of OpenTable being successful, I was trying to think of other industries where, if you put a network on top of [it, that] would absorb waste and make it more efficient and more usable. And the thesis of cars had come up, and we had met with several taxi [startups] — there were actually taxi startups before Uber. And we had quickly come to the conclusion that doing it on top of taxi wasn't the right way to do it because prices were fixed, they’re oligopolies, there's regulation, and if anyone did it on town cars, we would pay attention. So that was a thesis we had internally when they popped up.”

A short time before investing in Uber, Gurley had met with Taxi Magic, a leading ride-share company at the time, but was not interested due to its work alongside the taxi industry rather than working to disrupt it. Gurley wanted something completely new from the taxi industry, free from regulation and a true marketplace.

Eventually, Benchmark found Uber and quickly cold-called the co-founders Travis Kalanick and Garret Camp to meet. Benchmark passed on the seed round, however, because neither co-founders wanted to be CEO, and Gurley felt they weren’t totally all in despite being great entrepreneurs. Kalanick had founded and sold his company, Red Swoosh, and Camp had founded and sold his company, Stumbleupon, a few years before Uber. They were proud of Uber and saw a big vision but weren’t fully committed, which is certainly a red flag to an investor.

Another Benchmark partner, Matt Cohler, whom we mentioned earlier, became the number one rider of Uber over the next few months. He loved the product, and Benchmark continued to monitor it heavily. Four months after raising their seed round, Uber announced they would be raising a Series A round.

By now, Kalanick had become the CEO, and Camp was more involved. The one question that gave Benchmark concern was answered, and they aggressively pursued the deal.

There are two funny stories that show just how aggressively Benchmark was with Uber. First, they knew Travis was pitching to Sequoia the same day he was pitching to Benchmark. Kalanick, obviously, had taken an Uber to the Sequoia office and asked the driver to wait outside, which should be fine because no one in Mountain View would likely call an Uber. The partners at Benchmark, however, to mess with Kalanick, had called that same Uber to the Benchmark office leaving Kalanick stranded and having to run to the Benchmark office from Sequoia to deliver his pitch.

The second story is after Kalanick pitched the Benchmark team, they put him in another room at the office and told the receptionist to not let Kalanick leave until the partners were done creating the terms of the investment. They discussed briefly and then brought Kalanick back into the room to finalize a deal.

Kalanick, known for being incredibly aggressive, loved the pursuit by Benchmark. He tells these stories in an interview with a smile because he and Benchmark both shared that passion for making Uber a world-changing company. He’s asked in that same interview why he went with Benchmark, and he simply says, “They’re the best… it’s not even a close call.” Great founder-VC fit. Obviously, not great Founder-VC fit in the long term, as many know, but that’s not what we’re going to get into today.

So why was Kalanick becoming CEO full-time the missing piece for Benchmark to invest? Well, one, he had experience running a company, but two, and more importantly, Travis was unbelievably driven to make Uber a successful company, which is a really important trait Benchmark looks for. They look for founders who are deeply motivated by the mission of the business. Current partner Sarah Tavel says,

“This stuff it's really freaking hard, like building a company that endures… It's a Relentless pursuit of excellence… You have to be so vulnerable and admit how little you know because you're constantly in the biggest job you've ever had like you're constantly growing being challenged.

All the things that you don't know or all the mistakes you're making, it's just part of being a Founder, being a CEO in particular. You have to have a drive that's going to get you through that mission. It’s one of the most important drives… just feeling so committed to the reason why you started the company in the first place and what your customer needs from you but there's another thing that I think creates that overdrive and it's that desire to win that pushes you.”

Now, after reading a lot about Travis Kalanick, he was certainly driven to make Uber a success, but I think it was more-so because he was such a competitive and vindictive person. He’s the type of person that when someone tells him he can’t do something, he immediately tries to figure out how to do it to spite that person and prove he can do anything.

There are few, if any, software companies that were harder to build than Uber because every city they launched in was met with intense scrutiny by the taxi industry. Uber had to fight so hard and never take no for an answer, and while being vindictive typically isn’t a virtuous trait, in challenging startups like Uber, it is almost a necessary evil.

Anyway, Benchmark moved so fast on this investment because this deal was years in the making. They had already built up this thesis that many marketplaces were left to be created. eBay built the one for collectibles, and OpenTable built the one for restaurants, so they were constantly thinking, where else can you put a marketplace? As mentioned, Gurley had ride-sharing as an idea and was actively looking for the right company. Once they found Uber, they already knew about the potential of the industry. All they had to do was be sold on the team to do it.

Former Benchmark partner Bill Gurley has a great quote when figuring out what industries can become online marketplaces when he says,

“So certain businesses are prone to monogamy. So babysitters are prone to monogamy, hair cutters, if you find a good one, prone to monogamy, doctors, dentists, if things are succeeding you're not changing and those businesses are tougher for marketplaces. Restaurants, you're prone to promiscuity. You go to your favorites, but you want to try new ones constantly. And so that's a very different dynamic for a marketplace.”

I’d assume, unless you’re filthy rich, you don’t have a personal driver. You don’t care who drives you around; you just care that you get to your destination quickly and at a fair price. Ride-sharing is prone to promiscuity.

So, at the time Benchmark invested, Uber was growing over 25% month-over-month and were in eight cities. The entire black car industry in San Francisco had about 600 cars, and about a year after Benchmark invested, Uber had surpassed that, so I’d assume they only had 50-100 cars or so in San Francisco based on their growth rate at the time. It’s fair to assume they had less than that in the other seven cities so we can assume they were in eight cities with about 500 cars serving customers. Quite different from Uber today. You’ll probably see 500 Ubers in an hour if you just stand on a busy street corner in a city.

So Benchmark had to have a vision to see what Uber could be. To see it grow from 500 drivers total to what it is today which is 5.4 million drivers doing about 250 rides a second is unbelievable. It was even unbelievable to Bill Gurley who led the Uber investment and sat on the board for many years. Not even the founders saw it.

In Uber’s first pitch deck that they used in their seed round, and I’d assume many of the slides in their A round when they raised just a few months later, they said how their overall market was $4.2b and growing a few percentage points a year. They calculated this based on the taxi and limousine service markets, which they felt they were an alternative to. Another slide along the same vein is one of their final slides in which their best-case scenario is $1B+ in yearly revenue.

Uber’s revenue in 2022 was about 32x their best-case yearly revenue number and about 7.5x their TAM just twelve years prior. So there is an insane amount of market creation by Uber that maybe only Airbnb rivals, but even Airbnb didn’t 7.5x the hotel industry market. That’s just ridiculous.

You can find the link to the pitch deck here on my website

So I’m going to go on a bit of a tangent, but one I think is really important. Typically, we talk about why investors invested in the companies they did at the time of the investment. While this has to do with market forecasting, it has to do with a 2014 piece Bill Gurley wrote about why Uber’s market has expanded so much and why it has so much more room to grow.

I think it relates because thinking about market expansion is extremely important as a founder. As we talked about with Sequoia last week, having a good TAM story is very important, and showing how your product and service can expand that TAM by unlocking something completely new will almost guarantee you an investment if your claim is reasonable. So this is kind of a thought exercise in that regard.

So, bottom line, it relates. Also, I think it’s really cool, and it’s my blog, so what I say goes.

So, first in the essay, Gurley cites a few reasons why Ubers are better than taxis, most of which I’m sure they realized at the time they made the investment. I’ll summarize them below:

Faster pickup times - an Uber in a city typically takes around 5 minutes, and you have a live tracker to see how far away your car is, allowing you to plan and allocate your time as you wish rather than waiting outside looking for a cab.

Coverage density - Uber drivers are based anywhere and everywhere, so it’s typically easier to get an Uber in a more suburban area than a taxi, and it’s especially easier in most cities.

Payment - you never think about payment when riding with Uber because your card is already on file, and payment is automatic. You can pay for 1000 rides by just taking a few minutes to upload your card before your first ride.

Civility - the duel-rating system ensures that higher-rated drivers are rewarded with more rides, and higher-rater passengers are rewarded with better drivers and faster pick-up times.

Trust and Safety - There is a record of every ride ever taken, and Uber can track, find, and monitor every ride to ensure ultimate safety for the driver and passenger.

Cheaper - Dramatically lower prices because as Uber scales, it can pay its drivers less because they’re getting more rides, so their per-hour rate remains the same even though prices are getting cheaper, which has no effect on the drivers and a massive positive effect for riders.

Scalable - most importantly, all of the six points above improve as more people use the service. Prices get cheaper, pick-up times get faster, higher rated drivers and users take more rides, and the platform becomes more secure. A true marketplace.

The next part of Gurley’s essay is the part I find really interesting and where the conversation about market expansion comes into play. After all, Uber 7.5x’d their TAM in 12 years. Again, unfathomable, so, why did that happen?

Well, Uber became an alternative to car ownership. There are a few reasons for this:

Fewer people driving cars

In 2008, less than half of eligible drivers aged 19 or younger had a driver's license, down from nearly two-thirds in 1998.

Young Americans increasingly prefer urban settings rather than suburban settings where cars are more needed. Therefore, people are spending more time and money on public transportation, and Uber is a cheaper and easier means of traveling within the density of a city. (In DC, I have to walk 15 minutes to the parking garage where I have to store my car. Not cool.)

Car ownership is really expensive and comes with its inconveniences.

Inconveniences:

If you drive somewhere, you can’t have a spontaneous drink with friends or colleagues because you have to drive home afterwards.

The unknown time it spends to park your car in a densely populated area can be extremely frustrating and wasteful of precious time.

Expensive:

Gurley cites a 2014 report, which, if anything, is more expensive now, that states the average cost of owning a car based on gasoline, insurance, raw materials, servicing/repairs, and the actual useful life of the car expensed over the years, is $9,000 a year.

So, if you live in a city and want to own a car, you’d have to spend about $9,000 a year to deal with the inconveniences listed above. And, as more people migrate to the cities, fewer people will want to buy a car.

(One more point that Gurley didn’t mention at the time but is apparent today is Uber rides as an employee perk. Many people in prestigious urban jobs can take Ubers to their office, which is fully expensed by the company. Major market expansion by Uber).

What’s crazy about this is that less car ownership benefits people in more ways than just paying less per year than what it would cost to own a car; it also decreases housing costs!

Gurley cites that in 2016, in a conversation with Kara Swisher, Houston had 4.5 parking spots per car. If you decrease that number to 2, there can be way more housing units available for people.

Uber, in a way, is a virtuous business, which is pretty funny.

I could go on forever because this is just so fascinating, but I’ll stop there. Check out the podcast episode if you want more rambling. That’s probably not a good selling point for the podcast. Oh well.

In 2011, when Benchmark led the Series A into Uber, they invested $11.5m for about a 19% stake in Uber. The exact amount Benchmark invested in the lifetime of Uber is unknown, however; they don’t have growth funds, so they can’t do too much follow-on investing. They also were diluted down to 11% at the IPO since Uber raised about $22b of private capital before their IPO, which is just insane. Therefore, I’m going to assume Benchmark invested about $25m in total into Uber. This number could be higher, but I doubt it.

How much they invested doesn’t really matter, though, because their stake in Uber at the IPO was worth about $9,000,000,000, and they sold about $900,000,000 worth of Uber stock to Softbank prior to the IPO, so they made just under $10,000,000,000 on this investment on likely $25m of invested capital.

Let’s look at some more numbers because this is just too crazy not to. The multiple on that investment would be 396x, and the IRR would be about 111%.

So yeah, Uber was a good investment.

I’m sorry, I meant to say that Uber was the GREATEST INVESTMENT OF ALL TIME.

Well, second best. I’d still go with eBay. I’m sure Benchmark is happy with Uber being second, though.

Why did Benchmark Invest in Riot Games?

If you’re playing the game of which of these three investments doesn’t relate to the other two, you would certainly pick Riot Games. eBay and Uber, as we read, are the most lucrative investments Benchmark has ever made. Benchmark has more multi-billion dollar outcomes like Snap, New Relic, and Confluent, which you can read more about on my website: allthingsvc.blog, but I wanted to take a different angle for the third and final company we’ll be looking into.

First, I’ll lead by saying this investment was in no way a fund-returner. It was certainly a great standalone investment, but in the venture capital word, many would consider this a double when compared to the grand-slams of Uber and eBay.

In 2008, Benchmark invested $3.5m into Riot Games for 20% of the company. In 2011, Riot sold to Tencent for $400m, yielding Benchmark a fantastic 184% IRR and a strong 23x, but a measly $80m ROI.

Again, great as an individual investment, but in venture capital, the goal is to invest in startups that will return more money than the entire fund because the majority of companies VC firms invest in will return no money, so the winners really need to win. The fund that invested in Riot Games was $425m, so the goal is to invest in companies with a $425m+ outcome. While Riot failed to meet that criteria and drastically underperformed eBay and Uber, there are ample lessons founders and investors can learn from this deal.

So, let’s set the stage a little bit.

Here is how former Benchmark partner Mitch Lasky described Riot Games when he invested.

“When I invested in League of Legends, there were maybe 20 people in the company and they had a wire frame. They had nothing playable. They had no metrics. They had nothing. I went in and Brandon and Mark had a background that wasn't necessarily the kind of background I look for in games' founders, number one. Number two, they'd never made a game before. Number three, they'd never made a game with the team they had assembled before. In my experience as a publisher, having published hundreds of games, these would've all been huge red flags.”

So, all red flags for Mitch Lasky. Also, for those who don’t know, Mitch Lasky is widely regarded as the best games investor of all time. He held a senior position at Activision, led the gaming company Jamdat as CEO to a $680m acquisition by EA, and invested in many successful game companies. If your company is flashing red flags from him, you really have some red flags.

But he did do the deal, obviously, so what happened? Well, once again, Mitch tells the story better than I could. He says,

“I went into the meeting thinking, "Okay, this is a courtesy meeting and 15 minutes, I'm out of here." 15 minutes into the meeting, I was thinking, "Jesus Christ, I am going to do this. I'm going to invest in this company. These people are so compelling. They are going to die to make this product and they know exactly what they're doing and they're able to answer all of my questions and anticipate my questions in ways that I couldn't have even imagined." I was like, "Bring me Steve Snow," who at the time was their executive producer, because I was like, "I need to talk to the guy who actually knows how to make a game." I want to spend an hour with Steve and I spent some time with him and he convinced me that these guys had their head screwed on straight. And I was like, boom and I green lit the investment.”

I love that quote. “Okay, this is a courtesy meeting and 15 minutes, I’m out of here. 15 minutes into the meeting, I was thinking, Jesus Christ, I am going to do this.” Peter Fenton has a quote that relates to this idea of always taking the meeting, even if it’s a so-called courtesy meeting. He says,

“I start with the premise emphatic, yes, let's meet, because I have and always will create time as much as it may impact. When I don't have enough time to take that next marginal meeting, I shouldn't be practicing.”

Good thing Mitch answered the request to the meeting with a yes because, apparently, this was one of the easiest investments he’s ever done because 15 minutes after meeting the founders, he was all in. It takes a very open mind to completely flip your mindset on an investment, especially one that apparently had all the possible red flags in your general playbook.

But the founders had an incredible insight that made perfect sense to Lasky. Okay, last time I use a Lasky quote here, I promise, but again, he tells the story so well. He says,

"I think part of the pitch that Riot made to me that made me convinced that it had a distribution advantage and made me willing to invest in it, was the way they understood the existing audience for Defense of the Ancients, which was a game that was a mod of Warcraft 3. They were going to turn it into a standalone product and relaunch it online with its own characters and own IP.

You could see that as a studio bet on a certain level, but they had identified this enormous pool of users who were playing Defense of the Ancients. There was this crazy pent-up demand for exactly what they were going to do because modding Defense of the Ancients and running it as a user, you to find an out-of-print copy of Warcraft 3, and go through all of these machinations.”

For those who don’t know, the game Lasky is talking about here turned out to be League of Legends, which today makes billions of dollars a year in revenue from virtual goods within their game.

I love the way Lasky describes this insight by the founders because it’s what many software businesses do; these founders were just bringing that to gaming. For example, David Sacks, founding partner at Craft Ventures, once said an easy way to start a SaaS business is to just see what crazy loops people are going through to make dashboards on Excel and just turn that into a standalone product.

The founders of Riot recognized that there was so much demand for this adjacent game off of the original game of Warcraft 3, and it was growing. It consistently added users, despite how hard it was to play because Warcraft 3 was out of print, so you had to get a used copy just to play a mod of the game.

They saw an opportunity to take that underserved user base and build a standalone game just for them that would enhance their playing experience and eliminate all the hoops they had to go through. Even better, they were going to use the now common but novel at the time, free-to-play business model.

Rather than users having to buy an expensive out-of-print copy of an old game, Riot would give users an enhanced playing experience with very similar game mechanics yet with original characters and IP for free. They would make money on virtual goods, which I’m sure many investors in 2008 would’ve thought was crazy, but Lasky, being the GOAT of games investing, saw this as a huge opportunity. He had seen this work with the game KartRider in South Korea and thought it could work with this game.

He thought it could work because League of Legends would immediately have a strong following. Thousands of players were basically users from day one; once they were aware of the product, they immediately fell in love. They would absolutely buy skins to make their characters look cooler or double xp potions to level up quicker and earn new rewards.

As a personal fan of the gaming industry, I think this is such an interesting investment. There are so many genius insights from the founders that led to a multi-billion dollar company with millions of loyal players. They took the challenging and bizarre dashboards out of Excel and into its own product, but doing it with something so creative as a video game is incredible.

I’ll close with one quote from current Benchmark partner Eric Vishria about how magical never-before-heard insights by a founder are. He says,

“having that insight. That's the part where you're sitting in the meeting, you're three minutes in, and the founder says something that you've never heard anywhere else. Nobody has said it, nobody's put a blog post down on it, it's an insight. That insight is the magic.”

Even Mitch Lasky hadn’t thought of this insight by these founders. It was truly unique and has been proven over several years and several billions of dollars in revenue.

Magic.

The Anti-Portfolio:

Another week, another exceptional list of investments from an exceptional VC firm. But as we discussed last week, nobody is perfect. Let’s discuss some notable misses by Benchmark. Once again, I could only find information on some companies. I suspect they passed on many more for reasons I don’t know, but here are some HUGE misses for which I was able to find some information.

Google:

Ouch.

Jeez.

This hurts.

Bill Gurley describes some reasons why they passed:

It was 1999, and search engines were still in an ultra-competitive environment with questions regarding whether their business models actually made sense. Many search companies were starting and failing consistently, and it was beginning to look pretty murky. There were still many questions regarding whether anybody could make a sustainable business out of search and if anyone could compete with Yahoo.

Sergey Brin and Larry Page were two Stanford PhD students adamant about being CEO despite never running a company before, which, in late 1999, was extremely novel and gave many investors pause, including Benchmark.

Despite these two concerns, the price was still remarkably high. Gurley also mentions how the founders were so confident in their product and their abilities that it actually gave the opposite impression to the Benchmark team that these guys were maybe overselling themselves and might not be as exceptional as they seem.

As a result, Benchmark pursued Google but kind of did it with a one-foot-in-the-door mentality. On the flip side, Sequoia and Kleiner were pushing hard to get a deal done, so Benchmark was never going to be able to invest if they didn’t pursue with that kind of rigor.

While all of those three points were refuted just a few years later when Google went public and continued to accelerate, they were somewhat reasonable points at the time. I will say, though, if Benchmark looked into the product as intentionally as Sequoia and Kleiner, they would’ve seen how it was a much better product than any other search engine available at the time and that their technology was far superior.

It seems like Benchmark focused too much on the surface layer of Google, which showed many concerns, rather than looking under the hood, which showed much promise. Maintain the what could go right mindset that Bill Gurley repeatedly states is so important in venture, and always engage the founders to learn more about the product.

Airbnb:

This one is tough because, similar to why Sequoia passed on Salesforce, it relates to price. Benchmark passed on Airbnb because they have a rule regarding how much ownership they take in a company. They are adamant that they get around 20% when they invest in a company because Benchmark only does Series A investments. Therefore, they need to get a large ownership position to outlast the future large growth rounds that will dilute their ownership.

Greylock led the Series A, putting in $7.2 million for about an 11% or 12% stake in the company, far from the Benchmark 20% target. I understand the idea of passing when it is so far from your target, but even if they got diluted down to 2.5% by the time Airbnb went public, they would still return over $2.5b, so I’m assuming they didn’t see that $100b+ IPO in Airbnb’s future.

If they did, I’m sure they would’ve made the exception because they target companies that can return the fund, which is typically around $500m.

Much like Google, if you want to invest in ultra-competitive companies, you can’t hesitate. You have to be prepared for when that company raises that you already know everything about their business and market on the outside, and once they show you their financials, you already have a number in mind on what you want to invest. Any hesitation gives your competitors a huge head start, which is, I’m sure, what happened with Greylock.

Facebook:

Here we go again.

I know we talked about Facebook in last week’s Sequoia essay, but I think there’s something interesting about why Benchmark passed that is different from why Sequoia passed.

Benchmark passed because they had invested in Friendster and were conflicted out. For those who don’t know, it’s common in venture capital to invest in a company in an industry and have to stick with that investment. If you invest in eBay, you can’t invest in Amazon; if you invest in Postmates, you can’t invest in DoorDash; and if you invest in Friendster, you can’t invest in Facebook.

Why? Well, the reason isn’t only because you picked your team and should be supporting your team but because Benchmark takes board seats on every investment. They can’t learn private board-level information about Friendster and Facebook; neither company would allow that. They’re direct competitors, and it would be impossible for Benchmark to keep all that information private.

The lesson here is that when you’re investing in a company, it not only has to be one you’re willing to back for ten years, but it also means you have to be willing to not invest in companies like it for ten years. That trade-off that doesn’t get discussed much in venture capital but one I’m sure happens quite frequently.

One caveat: if you’re a small-scale angel investor, I think this is less strict because you aren’t taking a board seat and won’t be given much private information about the company, if any.

Conclusion:

Anyway that is all for today’s post. If you want to learn about why Benchmark invested in other companies such as Snap, Instagram, OpenTable, and WeWork, head to the website. If you want to hear a different rendition of today’s essay you can listen to All Things VC on Spotify or Apple Podcasts. Lastly, you can follow me on twitter @justin_pryor_ for more nuggets of information.

Thanks as always for reading, and stay tuned for next week for another deep dive on why a historic VC firm invested in some of the historic companies they did. Hint: we’ve talked about them quite a bit so far.