Founders Fund

Why They're The Number One VC Firm You Should Learn From, and Easily One of the World's Best.

Intro:

Founders Fund is likely the most non-consensus VC firm in the industry. Sequoia founder Don Valentine said to target big markets; Peter Thiel said to target small markets. Jeff Jordan says he likes competitive deals as a signal of future success; Brian Singerman says if a deal is competitive, then it’s too late to invest in that industry.

The list goes on and on, but in this essay, I’m going to elaborate on some of the truly unique principles of Founders Fund that, truthfully, I find to be the way venture capital and startup investing should be. Today, we’ll cover:

Why to Target Small Markets

Why Competition is for Losers

Why Invest in Market Creators

Why all Investments need Supreme Conviction

Why Founders Fund’s Firm Building Thesis is How Venture Capital Should be

I have several quotes from key partners at the firm that emphasize why Founders Fund is drastically different than any VC firm you’ve studied, but one you probably will learn the most from.

But first, who is Founders Fund?

Founders Fund was founded in 2005 by Peter Thiel of PayPal fame, Sean Parker of Napster and Facebook fame (Justin Timberlake), Luke Nosek, and Ken Howery, both also of PayPal fame. Founders Fund essentially pioneered the “VCs as former founders” movement that is so prevalent today. Their guiding principle was to treat founders with the respect they deserve by ensuring them that they were in charge and never felt threatened by the VCs at Founders Fund, backed by a vow never to oust a founder. In 2005, these principles were very contrarian to the industry.

Their remarkable portfolio consists of SpaceX, Palantir, Stripe, Anduril, Facebook, Airbnb, Nubank, Rippling, Affirm, Ramp, Flexport, Spotify, and many more multi-billion-dollar companies.

Therefore, I encourage you to pay attention when reading about their investment theses because, clearly, they’ve had some remarkable success in practice.

1. Emphasis on Starting in a Small Market to Capture a Monopoly

If you’ve heard of Peter Thiel, then you’ve heard of Zero to One, and if you’ve heard of Zero to One, then you’ve read Zero to One. So, this concept may not be that new to you since it’s the Peter Theil mantra and the book's thesis, but it’s worth emphasizing to start this essay as the core foundation of Founders Fund.

“You're starting a new company, you want to get to Monopoly, how do you get to a large share of a market? You start with a really small market and you take over that whole market, and then over time, you find ways to expand that market in concentric circles. The thing that's always a big mistake is going after a giant market on day one because that's typically evidence that you somehow haven't defined the categories correctly, and it normally means that there's going to be too much competition in one way or another…

Go after small markets—often markets that are so small people don't even notice them. That's where you get a foothold, and then if those markets are able to expand you can scale into a big Monopoly business.”

Amazon didn’t try to be Walmart of the internet and sell everything; it started by being Barnes and Noble of the internet and only sold books.

eBay focused on cultivating transactions for collectibles such as Beanie Babies before expanding to everything else.

Facebook built the social network for Harvard students before building the social network of the world.

All of these success stories were a step-by-step monopoly progression. Facebook had a monopoly on Harvard student social network platforms, then on all college campuses, then the U.S., then the world. Had Facebook gone head-to-head with Myspace and Friendster from day one, it may not even exist today because social networks rely on network effects, as in the platform improves as more people use it, so if Facebook was just another general social network, they would’ve had a worse product than Friendster and Myspace because they had less users and therefore less activity.

By creating an exceptional product for a small group of users and then expanding, Facebook had a large enough user base to compete with the larger social networks by the time it became a social network for everyone.

Peter Thiel uses the green-tech bubble in the late 2000s as an example of how going after a large market fails. Every green-tech company in that era said their market was world energy consumption, which is trillions of dollars. Therefore, if they just get 1% of that market, they’ll be huge!

NEVER position your startup in this way; it will almost always fail. It’s too big of a market for a startup to reasonably go after.

Very few green-tech companies survived this bubble, but none as notable as Tesla. Why did Tesla make it out? Well, despite having much less funding than its competitors, Tesla started out to build a high-end electric car that was fast and stylish so a wealthy, earth-conscious person didn’t have to drive a Prius. Then, once they captured that high-end market, they expanded to make more and more affordable cars before becoming the most affordable car on the market.

That is how you win in a large and competitive market. You make it non-competitive by targeting one specific niche, then growing niche by niche, constantly giving you a monopoly. These are the companies Founders Fund backs and the strategy Thiel and his partners constantly promote.

2. Competition is for Losers

The other reason not to compete head-on with well-funded competitors in large markets is that sometimes that market is flawed, and everyone unknowingly competes to zero. Peter uses the following example.

“Competition can make people hallucinate opportunities where none exist. The crazy ’90s version of this was the fierce battle for the online pet store market. It was Pets.com vs. PetStore.com vs. Petopia.com vs. what seemed like dozens of others. Each company was obsessed with defeating its rivals, precisely because there were no substantive differences to focus on.

Amid all the tactical questions—Who could price chewy dog toys most aggressively? Who could create the best Super Bowl ads?—these companies totally lost sight of the wider question of whether the online pet supply market was the right space to be in. Winning is better than losing, but everybody loses when the war isn’t one worth fighting. When Pets.com folded after the dot-com crash, $300 million of investment capital disappeared with it.”

An obvious, more recent example is crypto. Everyone was building coins and all of them were getting so much funding. Therefore, a passive investor or a money-hungry founder may confuse that huge influx in competition in a huge market, the global monetary system, as validation that a market exists.

Now, crypto has its use cases, but there were way too many companies without compelling use cases raising money, which killed the market once interest rates began to rise.

You may not be surprised, but according to my research, Founders Fund only invested in Bitcoin in 2014, which it sold in 2022, right before the crash, before buying more in late 2023, at the bottom. Ridiculous market timing, first of all, but the point is, Founders Fund really practices what they preach. Bitcoin had a clear use case and a monopoly on the digital gold market, whereas all of the other coins were trying to compete with it or with Ethereum in a usually undifferentiated manner. Therefore, Founders Fund stayed out of the hype cycle and stuck with the monopoly market leader.

Not only does Founders Fund not invest in companies with high competition in their market, but they also don’t invest in companies where they’re competing for the allocation with other VCs. Partner Trae Stephens once said the following,

“There's something deeply troubling about prices getting out of control that has nothing to do with the price itself. Usually, what an inflated price means is that the deal is being competed, and so the founder believes that they have leverage. The worst deals are the most competitive deals because they're the ones that are super consensus: everyone agrees on the thesis, everyone agrees on the founding team, and there's no edge on the investment. Everything is going to be expensive at every round so your expected value is going to decrease, and it usually indicates that there's some mimetic contagion that's happening in the marketplace.

So when a founder says I'm going to let this run auction-style, they're actually saying secretly inside their head, all I care about is competition, and I'm just going to let it run, and I'm going to take the best price at the lowest dilution that I can accomplish, and I don't care that if that impacts the long-term responsible growth of my business.”

Founders Fund avoids these high-priced auction-style investments by fully avoiding the hype-cycle deals.

So, if they pass on all of these companies and all of these hype cycles, when do they invest? What’s their actual investing strategy?

The goal of Founders Fund is to invest in the companies that create the market and create the hype cycle.

3. Invest in the Creator of the Space, Not the space itself

In great timing with this essay, last week Trae Stephens wrote a rare blog post about why Founders Fund only invests in market-creating companies and why most VCs follow herd behavior.

“The average investor does not spend all day simply searching for the best new company; they spend all day searching for the best new company in a socially approved technology “space.” Twenty years ago, that space was e-commerce, the “dot.com”-ing of brick-and-mortar stores. Fifteen years ago, “social-mobile-local.” Ten years ago, the “sharing economy.” Three years ago, gaming and crypto. Now, it’s artificial intelligence.

This herd behavior is not harmless.

A hyped venture space only exists after the winning company in that space has already been created, discovered, funded, and become popular. The very existence of the space proves the search for a winning investment is already over. This is the reality of venture investing, and the herd behavior operating in open defiance of this reality is necessarily limiting fund returns while denying capital to promising companies simply because they aren’t on trend…

Instead of evaluating pitches on a relative standard — “How does this particular AI start-up compare to all the other AI start-ups?” — VCs should use an absolute standard. Relative wins are effectively irrelevant to the returns of any large fund. The real question to ask is: “Could this company become a category-creating monopoly? Could it come out on top of the power law?” Because those are the only companies that matter…

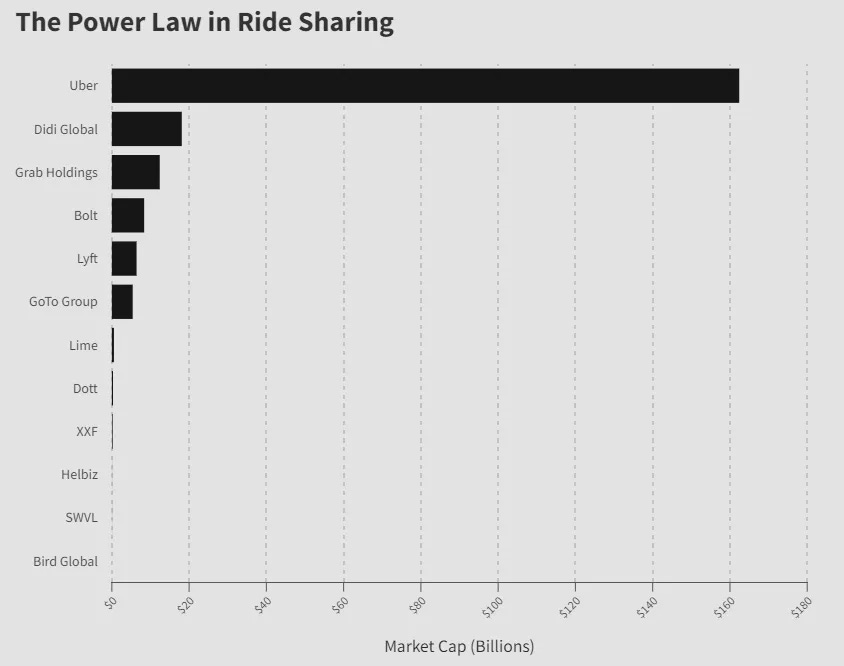

"Uber wasn’t just a unicorn, it was the creation of a new investment category… And yet, fifteen years later, Uber is still the dominant player. At $162 billion, its market cap is triple that of the next ten ride-sharing companies combined.

This is the power law, and it’s remarkably consistent across product categories. At $47 billion, Coinbase’s market cap is more than double the next ten crypto companies combined. At $180 billion, SpaceX’s market cap exceeds that of the next twenty space companies combined. And at $1.2 trillion, Meta’s market cap is more than double the next dozen social media companies combined.”

I touched on this in my Five Things I Saw Last Week post, so sorry if I’m being repetitive, but I could not believe just how much larger these market-leading companies were compared to their closest competitors. I mean, one company being multiples larger than several of its competitors combined is insane and can only be done by market-creating companies.

This power law effect is why Founders Fund claims they should only invest in market-creating companies even if the loss ratio is twice as high on those investments because the outcome is so huge.

Let’s say Founders Fund invested in a few companies trying something new in bio, agriculture, energy, robotics, and space in 2008 vs. a fund investing in various social networks and consumer marketplaces. Maybe that generic VC fund returned a 4x and $500m total because perhaps they had a few 3x returns or a 5x and even got a nice 50x on Instagram or something.

Founders Fund, on the other hand, could lose all of their money on four out of those five companies in those unique and difficult industries, but that one hit in space with SpaceX is currently worth about $18.75 billion and will probably be the greatest venture investment of all time when SpaceX finally goes public. Therefore, in this example, Founders Fund vastly outperformed the VC firm that even had a great outcome following this herd behavior, whereas most firms following the herd behavior underperform.

And maybe you’re thinking, well, you just gave an example with SpaceX. Obviously, they’re going to outperform, but they’ve done the same thing with Anduril, and Flexport, and Palantir, and so on—non-consensus moonshots against the consensus point of view.

Founders Fund plays the grand slam style of venture capital: Invest in moonshots that will likely fail and lose money on more investments than the average VC firm, but invest in the companies that become monopolies in a growing market by creating something truly revolutionary.

Another way to say that Founders Fund doesn’t follow herd behavior is to say that Founders Fund makes non-consensus investments. Brian Singerman describes their non-consensus strategy as it relates to the present funding environment as follows,

“In 2023, AI, by definition, was the least contrarian possible thing you invest in. Right? And so we just take our strategy of we're just gonna invest in the best thing, put a lot of money in OpenAI, call it a day. But one of the things that we've started to do really, really well, is if everybody is chasing after this stuff, let's go for things that we still believe in but that are not necessarily that consensus. So we hired Joey Crowe. Like, the best crypto investor in history. He's amazing. And he's doing all the best crypto stuff because crypto is less hot now Fine. Great. Take the best assets; invest in them.

I don't do very many deals now. When I do, I try and sink my teeth into one. We're doing Ohalo with (David) Freidberg. It's just a space that's ridiculously important: bioengineering, gene editing, agriculture. It's gonna be one of the most amazing companies on the planet, not AI. And so we try and find these things with amazing founders. That part doesn't change.

You find people you know well who are doing things in contrarian spaces that in 3 years will not be contrarian. Like, bioengineering for agriculture will not be contrarian in 3 years.”

I love that.

2023 was the year of AI. All ANYONE ever talked about was AI, and here’s Founders Fund investing in crypto and agriculture. I bet in ten years, those investments are going to look fantastic.

So Founders Fund invests in non-contrarian companies, but that doesn’t mean they predict the future, as a16z’s Chris Dixon (an incredible investor) loves to talk about. Founders Fund leaves the predicting the future part to the founders.

They have the industries they prefer to back, but they let unique founders lead the way. They aren’t thesis-driven in the sense that they look for companies building in the areas they think will be big; they’re just putting a beacon out to the world that if you’re a non-contrarian thinker building something non-contrarian, then come talk to us.

Trae Stephens explains this well as he says,

“Your investment thesis is only as good as the strength of the companies that come and pitch to you. Did I have some super crazy interest in supply chain and logistics or a thesis in supply chain and logistics before I invested in Flexport? No, of course not. I needed Ryan to convince me of the timing of the market.

I think that anytime you're looking at a thesis about the future, you are saying there is a category, and I have some belief in that category, that means you're probably too late. If you have a thesis on Space Tech but you're not a SpaceX investor, you're probably losing money. If you have a thesis in crypto but you're not in Bitcoin and Coinbase, you're probably losing money. It turns out that the core monopoly investment that won is the only one that mattered; the rest of the category matters a lot less. So if you have some vision for what the future looks like and you're looking for a company to invest in that's doing it rather than starting it, you're probably already too late.”

As I said before, Founders Fund invests in the companies that create the market and create the hype cycle. They do that by letting the founders tell them what’s next. Ryan Peterson of Flexport, for example, spent years in China shipping cheap ATVs to the U.S. and learned everything about shipping and all of its inefficiencies. That’s what led him to start Flexport. Founders Fund (and basically any VC) will never have the kind of insight that a founder like Ryan Peterson has in an industry because they’re meeting every day with different founders, building different things. It’s impossible for them to be experts in any one industry.

Therefore, Founders Fund doesn’t have an industry thesis. They let the founders come in and tell them why they’re creating an industry, and if that founder is eccentric and the story is compelling, they’ll go all-in.

4. Extreme Conviction on Their Investments

Extreme conviction was a founding tenant of Founders Fund that the team practiced to the fullest extent. Not only were they the only institutional investor in SpaceX at its first funding round, but they put in $20m when all of the rockets had blown up. That’s trust.

Even crazier, Luke Nosek put his parents’ entire retirement fund into Facebook in 2007! So, yeah, they really really have conviction on their investments.

Brian Singerman carries this principle through the firm today as he says,

“I just have the tolerance to go all in on those bets. Like, if I see an awesome founder and I've hung out with the awesome founder and strategized with them, I'm willing to put a large portion of the fund into those companies.

I don't think that’s a standard thing in venture capital. Like, most funds have 3% of fund checks, 5%. I mean, one of the things that we've done really, really well over the years is 20% of the fund check. Our 3rd fund, we put 33 percent of the fund in Palantir; we've done those bets historically.”

33% of one fund into a company is absurd and almost certainly has never been done by any other VC firm. I’ve discussed many times in this blog how venture capital is so high-risk that most VCs diversify their portfolio across 20-30 companies at a minimum, usually with equal investment amounts into each company. For Palantir, Founders Fund put 8-12 investments worth into one company! Talk about conviction.

They also did something similar with Airbnb, putting $100 million out of a $500 million fund (20% of the fund) into the company. Con-vic-tion.

Additionally, whenever they have a company they’re all-in on, which is typically most of their investments since that’s basically a requirement to invest, they invest across multiple funds. Founders Fund has invested several rounds in Palantir, Airbnb, and SpaceX. Again, basically, any chance they get to put more money into a company they’ve backed, they will do so.

Therefore, it’s no surprise that Founders Fund owned about 5.5% of Airbnb at the IPO, about $5.5b of value, 12.7% of Palantir at the IPO, about $2.5b of value, and currently hold about 10.4% of SpaceX, about $18.75b worth of value at the $180b valuation the company had in December of 2023. As I said, Founders Fund's investment in SpaceX will likely be the best venture investment of all time, and it’s all because of their conviction. They’ve invested in SpaceX across four funds, and I’m sure they will continue to do so.

Since so much money goes into these companies, it’s really hard to get a deal done within the partnership because it’s not just a 3% of the fund investment; it’s a 10, 20, or even 30% of the fund investment over that company's entire fundraising lifecycle. Trae Stephens elaborates on this as he says,

“Everything is super difficult to get through the investment team and this is on purpose. The rough thesis is that the more process you have, the easier it is to game the process and get to some mediocre outcome.

I'll give you an example. Say the most junior person on your team meets with a company and they're like, yeah this company's pretty good, I like the founder, I kind of like the idea, I'm gonna have them talk to a principal or a partner. Then that meeting happens and they're like, it's interesting. I don't have like super high conviction, but we'll bring it up at the partner meeting on Monday, and then the GP is like yeah, let's do a meeting with him. By the time that it gets to that point, it's like okay, maybe we don't have the conviction to write a big lead check, but maybe we put something in because it made it all the way through the process, so you know, this is probably worth a participation check.

Our approach to this is that it's going to be really hard to get anything through because there's no structure set up to get it through. It's just personal willpower to go and convince people to take the meetings outside of this process cycle. In order to get anything through, you literally have to just be pounding the table. It is on you to have the level of conviction that's required to get people on board.”

I’ve heard many VCs talk about the process of a deal getting done: an associate sourcing the deal, then passing to principles, then passing to the partners, but I’ve never heard it from this lens, which I thought was pretty interesting. Obviously, I’m sure all VCs who conduct this process will disagree with Trae, but I’m sure there’s some truth to that claim that something good rather than great can get through because it has gotten passed along enough. It’ll get the benefit of the doubt.

I also think the point he made about participation checks is a big reason for this. Since VCs typically invest in so many companies, they write a lot of checks, which can waver in size. Therefore, since they have a target investment amount per fund, they need to get to, again, maybe 30 investments. Some of those very well could be a small check just to say well, it seems good enough, so might as well.

Since Founders Fund backs up the truck across multiple rounds on all of their investments, they’ll never let an investment go through that doesn’t have supreme conviction. That’s why every partner can lead a deal, but that one partner who’s leading the deal has to absolutely pound the table, saying he or she will resign if they don’t do this investment because he or she believes so strongly in it.

While the conviction of each partner around each investment can wane, the necessary outcome of that conviction never changes, as described by Peter Thiel,

“The biggest secret in venture capital is that the best investment in a successful fund equals or outperforms the entire rest of the fund combined. This implies two very strange rules for VCs. First, only invest in companies that have the potential to return the value of the entire fund. This is a scary rule because it eliminates the vast majority of possible investments. (Even quite successful companies usually succeed on a more humble scale.) This leads to rule number two: because rule number one is so restrictive, there can’t be any other rules.”

Fund returners 👏 Fund returners 👏 Fund returners 👏.

5. Why Founders Fund’s Firm Building Thesis is How Venture Capital Should be

Not only does Founders Fund invest in a unique way, but they also operate their firm in a unique way.

Most notably, Founders Fund encourages partners to go start companies if the firm believes it is the best way to generate returns on an investment. Trae Stephens co-founded Anduril with Palmer Lucky because they built a relationship when Founders Fund invested in Palmer’s first company, Oculus, and when Palmer was kicking around the idea for Anduril, Trae loved it and went all-in to help him. He’s still a partner at Founders Fund but dedicates a lot of time to Anduril because he believes that’s the best way to generate returns for the firm. So far so good because Anduril is currently worth about $8.5b, and Founders Fund likely owns at least 10% of that.

Similarly, partner Delian Asparouhov started Varda within Founders Fund and is seemingly on its way to unicorn status after some hugely successful test flights.

I think this thesis should be the general thesis of venture capital. This was one of the theses of Tom Perkins and Eugene Kleiner back in 1972 when they started Kleiner Perkins; they wanted to populate the firm with partners/EIRs to invest and then start a company when inspiration came. That is why John Doerr joined back in the 1980s; he wanted to start a company one day, and Kleiner Perkins gave him the green light. Though, I guess he was too busy becoming one of the greatest venture capitalists ever to get around to that. Cough, Amazon. Cough, cough, Google.

Regardless, this strategy has lost its thunder in modern venture capital, but Founders Fund emphasizes it strongly. I am shocked that more firms don’t emphasize this because it clearly works well for them.

Now, this thesis can only work if Founders Fund hires exceptional people who are brilliant in a certain domain. Brian Singerman describes this strategy as the following,

“One of the things I think we've done really well is our hiring. We've been able to focus our hiring on people that come in, and have a truly unique angle or moat that makes them special. Whether it's in the sourcing, picking, connections, getting in, anything, if it's a unique strategy that is differentiated from the current partners that are here, we are interested in hiring that person and that's really paid off.”

If you hire someone like Delian, a super-genius MIT dropout, chances are he’ll do something impactful for the firm. Did they expect him to start a drug manufacturing company in space? Probably not, but they knew he would do something remarkable because he’s in the 99.9 percentile in his domain. Thus, exceptional hiring, as with most firms, is really at the crux of Founders Fund success.

I often forget that VC firms are actual companies. This might sound dumb, but I mostly just think of them as traders buying and selling stock in companies. Founders Fund actually feels like a company to me because they focus so much on hiring and empowering their employees to take risks and do interesting things. They really care about building firms internally and supporting world-changing companies externally. Again, this is how I think venture capital should be.

They mold these young associates or principles to become future partners or founders by really throwing them in the deep end. Everyone is empowered to make investments, even associates, make many mistakes, learn from them, and constantly adapt their mental frameworks. This is put into practice by the team requiring new hires to take tons of meetings when starting (Trae Stephens said he took 500 meetings with founders in his first year alone).

So, the autonomy to go out and do interesting things, the leeway to make mistakes and learn, and the sheer effort required of new hires within the firm really cultivate this environment of learning, excellence, and impact that eventually will accrue in one way or another through leading incredible investments or starting world-changing companies.

So, How do You Land an Investment from Founders Fund?

So now you know how Founders Fund invests. If you’re a founder and want the support of a fund that will write multiple huge checks into your company while never telling you what to do, then there are a few things you need.

You need to be a master of your domain, a supreme outlier, a ruthless operator, and a visionary.

You need to build a company that is so precinct and novel that it will create an entire industry off the back of it.

You need to make a compelling case that you can be at least a $10 billion company, though $100 billion will be better received.

You will face minimal competition throughout the growth of your company by constantly monopolizing niches before expanding.

You have to be so non-consensus that you barely mention AI in your pitch, if ever, but on a more serious note, you have to be building something that people will think you’re crazy for doing, but you know you’re right.

If you check these boxes and can make a compelling case why you do, you have a strong chance of raising from Founders Fund.

I’m sorry to inform you that this won’t be many of you, but if you think you fit the bill, PLEASE LET ME KNOW.

I hope you liked this post. If you did, give it a like! It helps the blog out a lot. Also, subscribe to see future interesting posts like this, including this Sunday, for five interesting things I saw this past week. You can check out last week’s post here.