Initialized Capital

Initialized Capital

Why Initialized Capital Invested in Coinbase, Instacart, and Rippling, and Key Lessons from Former Managing Partner Garry Tan

Brief History:

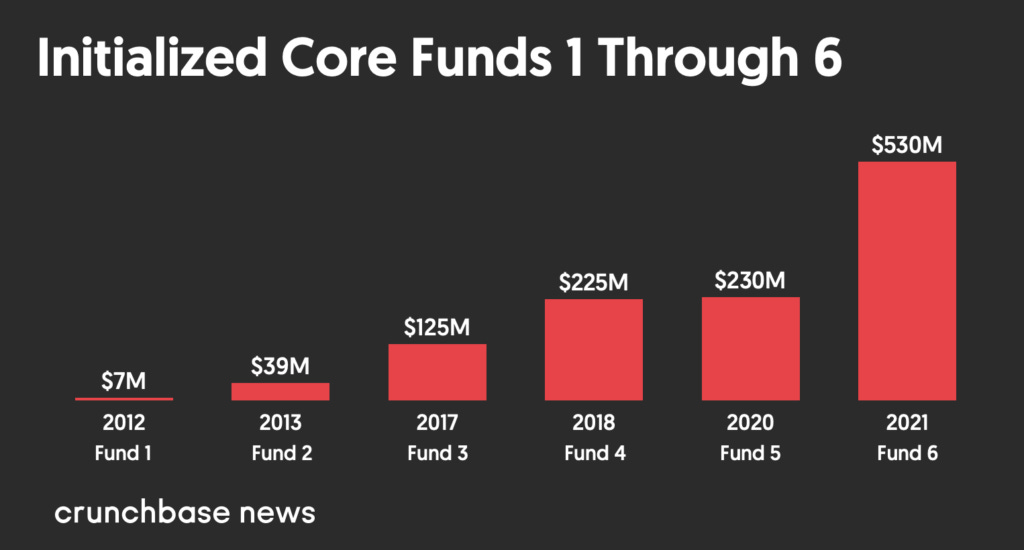

It’s rare that a Venture firm invests in 27 unicorns in just 12 years of its existence. It’s even rarer that a venture firm invests in 27 unicorns all at the seed stage, even when it’s just a founder and an idea. It’s EVEN RARER that a firm turns a $7 million fund into over $2 billion in distributed capital for LPs.

Put all of those rare feats together, and you get one of the best, if not the best, early-stage VC firms: Initialized Capital.

Garry Tan, Alexis Ohanian, and Harjeet Taggar, all YC-backed founders, started Initialized Capital in 2011. While Ohanian and Taggar left a few years ago, Garry Tan recently left to rejoin Y Combinator as its CEO, leaving Initialized partners Brett Gibson and Jen Wolf in charge of running the firm.

Since its founding, the general thesis of Initialized, as described by founding partner Garry Tan, is as follows:

“The coolest thing about initialized has always been being able to believe in Founders before it's totally obvious because that literally is what you have to do in order to create returns that nobody else can get. You have to believe in Founders maybe when they just have a demo, and they have an early idea that there's a problem that we could solve.”

That is how you can achieve billion-dollar returns on less than $7 million of invested capital – by backing founders at the earliest possible stages – the highest risk taken for the highest reward.

In this essay, we’ll look into many principles Initialized has of backing builders, backing founders they’d want to work for, and attacking an opportunistic market with a very non-consensus idea. These theses, among others we’ll explore today, led them to invest in 27 unicorns, including Flexport, Cruise, Opendoor, and Patreon, among three other companies valued at over $7.5 billion, which we’ll discuss today. These companies are a few reasons why Initialized is regarded as one of the best pure seed-stage investors of all time and is quickly growing.

Today, we’ll investigate why Initialized invested in Coinbase, Instacart, and Rippling. We will also dive deep into the firm’s general investment theses, what they look for in founders, what traits make good VCs, and some general advice they have for founders. At the end, rather than our traditional Anti-Portfolio format, since either Initialized has no major mistakes or just has never spoken publicly about them, we’ll explore three mistakes Garry Tan has made personally in his startup journey that include key lessons for founders from a first-hand experience.

Before I get started, I want to mention the podcast. You can listen along or separately if you prefer.

Let’s jump in.

Why did Initialized Invest in Coinbase?

If you think crypto isn’t as popular as it should be today, imagine what it must have been like in 2012, just three years after Bitcoin was released in 2009.

Very few people knew what Bitcoin was, and most who did thought it was interesting but probably not useful long-term. Garry Tan, however, believed in Bitcoin's potential due to his concerns with the reliability of fiat currencies. When he tried to buy Bitcoin before Coinbase started, he had to use a website called Mt. Gox, which provided a horrible experience that left many users not even trying to buy Bitcoin, even if they were interested.

Initialized has had so much early-stage investing success because one of their founding principles is anti-mimetic (unique perspective; not like others) investing. Former Managing Partner Garry Tan describes this thesis as,

“We often ask ourselves, what do we believe that nobody else believes? We ask the founders that too. If there isn't one of those things embedded in an anti-mimetic aspect to the business, often we don't want to fund it.”

Well, Brian Armstrong, founder and CEO of Coinbase, believed that this coin, with less than a $150 million market cap, could eventually become a new gold standard and the foundation of a global currency without government intervention.

That is quite the anti-mimetic thinking there.

The U.S. Dollar, Euro, and Chinese Yuan have trillions of dollars in circulation, backed by decades of staying power, government and militaristic support, and global user adoption. How was a digital coin known by less than a million people in the world supposed to uproot that?

Again, a digital coin.

But like I said, Garry believed in Bitcoin as well, so he appreciated a fellow non-consensus thinker and was intrigued by Brian’s initial cold email by sending Garry 0.05 Bitcoin, worth about $0.23 then compared to about $2000 today, using his service Bitbank, now Coinbase.

First, that’s a great cold email because it essentially was a very quick and simple demo of the product Brian built to transact Bitcoin, which seemingly no other companies were building or could effectively build. It made Garry wonder, if all goes well, if Bitcoin is adopted globally as Brian Armstrong believed it could be, what would Coinbase look like?

We’ve talked about having this optimistic viewpoint of the world when investing in startups previously in this blog, but Initialized has used this principle in every investment they’ve made. Tan once said,

“The way that we try to approach it is to suspend disbelief. When Brian Armstrong came in and said we're going to upend the global financial system with something that is open and the blockchain, it's very easy to look at the total ARR of all of this cryptocurrency stuff is sub a billion dollars. This is very fringe. Look at what Wall Street Journal is saying. You would just say no on the spot.

But if you come at it with a different angle, which is if what this person is saying is true, what would happen? One thing I like to ask is would we choose to live in that world?

So obviously, Tan wanted to live in that world and could see the potential cryptocurrency had if all went well. I mean, global currency transactions are obviously a multi-trillion-dollar market, so there’s quite a massive reward potential if Armstrong’s thesis approaches reality.

So, the idea is crazy, and the market has outlandish potential. Maybe this is worth a seed investment. After all, VCs, and especially Garry Tan, are conditioned to think about what could go right.

But it’s not just about the idea and the market. As we know, at the early stage, it’s mostly about the founder, so what about Brian Armstrong made Initialized think he could be the one to make this vision a reality?

What’s interesting is that Brian Armstrong was by no means a Vitalik Buterin type who studied crypto for many years before starting a vital piece to the ecosystem by creating Ethereum. Armstrong actually worked in the anti-fraud department at Airbnb before it was even a $1 billion company.

He was just curious enough to explore this idea further and used his engineering abilities in security to build an exceptional product, the MVP of which he built in just a few weeks.

Interestingly, seeing a founder create founder-market fit is more exciting to Initialized than someone with natural founder-market fit. Current Initialized Managing Partner Brett Gibson describes why this is such a bullish signal as he said,

“There's always this concept of founder market fit, and in some technical domain, sure, you need to have worked a long time and Rockets to create new rocket engines, but I think there's a wide swath of the opportunity for very smart technical people to will themselves into founder market fit.

To learn everything about a market. We get Founders that are talented and second-time Founders, and they just pick something entirely different, and they go out, and they just make sure they know everything about it, and they just decide to become experts and decide to have fit for a given Market.”

It's remarkable that Brian went from an enthusiast to a full-on creator of a platform that services this need in a few weeks. Think about what he could do with years of effort on this project if that’s what he could do in a few weeks!! It’s a remarkable signal that showed Brian had strong potential as a founder to build something world-changing.

Initialized also received some budding proof of product-market fit when Coinbase was growing 20% a day just five weeks after launching. A DAY! Every four days, they were doubling. I’ve never heard of a company growing that fast, even at the minimal level that Coinbase was growing from.

Through the combination of backing anti-mimetic ideas by a founder that created founder-market fit to tackle a problem with world-changing potential in the trillions of dollars of value, Initialized invested $300,000 into Coinbase’s seed round after YC Demo Day. They would invest about $1,300,000 total into Coinbase, giving them about a 2-2.5% ownership stake at the time of the IPO, which valued their investment at nearly $2,100,000,000 for about a 127% IRR and a 1,606x multiple!

Unbelievable numbers with ROI multiples that we will likely never explore again in this blog (We aren’t peaking, I promise). It really goes to show that being non-consensus and right has potentially world-changing outcomes, which again just explore the beauty of venture capital and how much value small sums of invested capital can create.

Why did Initialized Capital Invest in Instacart?

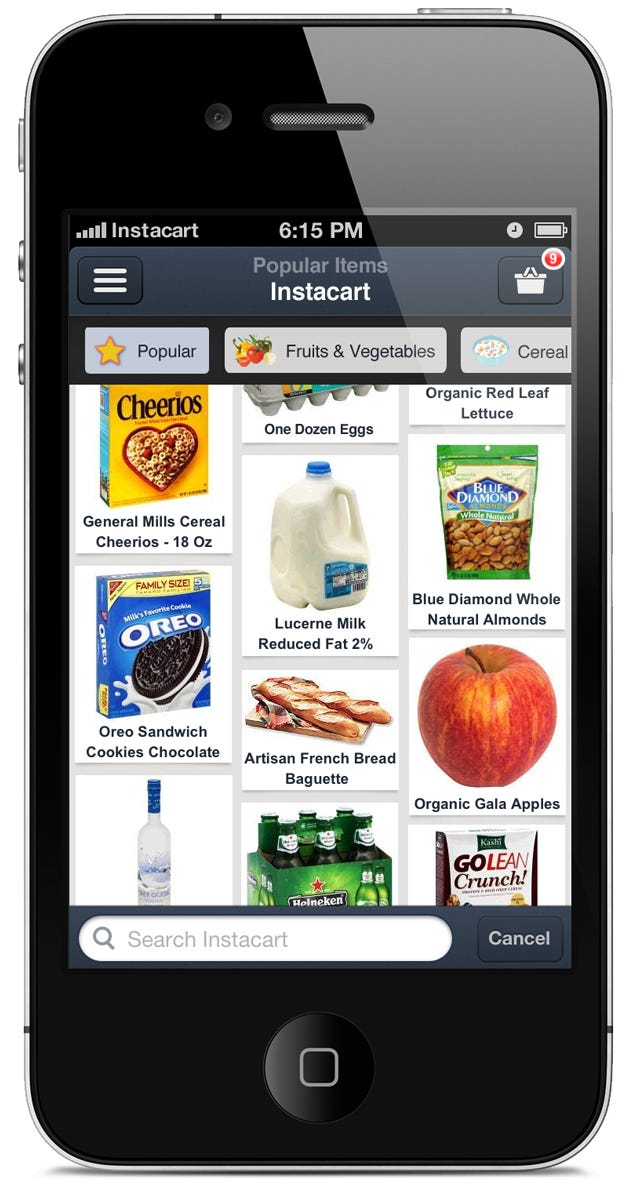

Garry Tan’s introduction to Instacart is legendary. Garry was a partner at Y Combinator when he started Initialized Capital. While at YC, a founder, Apoorva Metha, emailed Garry asking if he could get into Y Combinator. Tan told him that the deadline had passed, and it would be nearly impossible to get him in now.

Metha took that as an opportunity to showcase his business, Instacart. To prove he had something special, he found Garry’s address at the YC office and sent him a six-pack of beer using his app. This exceptional cold email/product demo is another incredible example of effectively pitching a VC firm however you can. Much like Brian Armstrong did by sending Tan some Bitcoin, unique intros like that show VCs you have hustle, confidence in your product, and a product that does what you intend it to do, which isn’t always the case at the seed stage.

This was especially notable for Instacart. Uber had been out for almost two years and was growing like wildfire. People could tell the gig economy was going to be big. Grocery-delivery companies like Instacart were pitching their ideas to investors, but that’s all they were – ideas.

It was such an initially capital-intensive business model that any startup that tried it would initially lose a lot of money. In fact, in the early days, Instacart was burning $30 to make $12. That’s atrocious unit economics! Despite that, however, Apoorva built out the app himself and hired a few drivers on Craigslist to pick up the groceries when he was alerted of an order from the Instacart app that Metha was updating with pictures of groceries daily that he bought from the store.

It wasn’t the most efficient process, but it showed that Apoorva was willing to test his thesis through a product rather than a pitch deck. Initialized President Jen Wolf talked about why founders like this are so appealing as she said,

“They're people who like to build things to solve problems, right? They don't want to just talk about it or research it, they are very action-oriented, and they said like I've identified this problem, and this is how I'm going to start to figure out how to get product market fit or how to solve the problem. I'm going to create a product and put it out there, and that's going to be my main way of trying to understand whether this is something people want or need or like to what to create.”

So, the founder aligned with Initialized’s thesis: a builder willing to prove his hypothesis and scrappy enough to make it work himself and prove it to investors. Obviously, no VC would invest in a company with those unit economics, but once Instacart reached sufficient demand to build out its actual gig economy and start its ad network, it would be profitable, as we see today.

But that wasn’t obvious at the time. A lot had to happen for Instacart to get there, and honestly, I’m not sure they ever would’ve without the ZIRP environment.

Regardless, Initialized funded Instacart because the company aligned with Garry Tan’s “Three Whys.” He described them as follows,

“Technology, behavior change, and government regulation. I want you to keep those in your mind as you evaluate any startup idea. Those aren't the only three, but those are the ones that I have seen up close, and we funded dozens of billion-dollar startups that have made it based on those three.

Watch for the curious and interesting intersections between very large things. Look for the points of contact or points of conflict. Pick two enormous forces and wonder how they connect. And where those intersect is the one big question, why now?”

Instacart started at the perfect time, coming off the heels of Uber. First, mobile smartphones created the opportunity to order, track, and deliver groceries. Second, behavior was changing in the gig economy, becoming a place where regular people could easily pick up a second or full-time job, and people were getting more comfortable paying a premium on ordering things to be delivered to save time. Lastly, Uber fought hard against government regulation for Instacart, allowing the gig economy to be a thing in the first place.

Instacart started at both the perfect time and probably as late as they possibly could because, typically, when the three whys intersect, it is the best time to start a company, and that becomes more obvious to everyone else by the day.

Since Apoorva was a builder willing to test his thesis through an extremely compelling pitch by sending Garry Tan the six-pack of beers and earning the badge of the latest YC applicant to be admitted, and Metha’s timing of building Instacart at a time when Tan’s three whys were perfectly intersecting, Initilazed invested $150,000 into Instacart’s seed round.

Reportedly, Initialized did no follow-on investing, which they typically do not do, and therefore only had around a 0.2% ownership at the time of the IPO, making their stake worth about $17,000,000 or, if they sold in the last private fundraising round, which valued the company at $39 billion, their stake would’ve been worth about $74,000,000. Regardless, it may not a major sum compared to their Coinbase investment, but at the IPO valuation, they did achieve a 54% IRR and a 113x, which is a multiple many firms would kill for.

Also, this was out of a $7m fund, so 2.5x the fund is certainly a great investment, or a 10x on the fund, depending on when they sold.

Why did Initialized Capital Invest in Rippling?

Some of you may not have heard of Rippling for two reasons. First, it’s not a public company, but it was valued at $11.25 billion in March 2023, so it might as well be. Second, it’s an HR and IT software company, so it’s not the most exciting product.

But obviously, an $11+ billion valuation is no joke, so how did this company go from $0 to $11,000,000,000 in seven years?! And how did the Initialized team once again find a diamond in the rough?

Well, the first thing that appealed to the Initialized team was that Rippling was bringing software to HR and IT, an industry with many manual processes that hadn’t been automated by software yet. Initialized’s Jen Wolf describes the firm’s thesis on this premise as follows,

“Find companies building software solutions and industries like manufacturing, grocery, and freight. Industries that might still be using paper or email or old Excel sheets. Sometimes you call those file cabinet businesses because they've got all the paper around to do things. So, those are companies that need to adopt technology in order to stay competitive and innovate in their industries.”

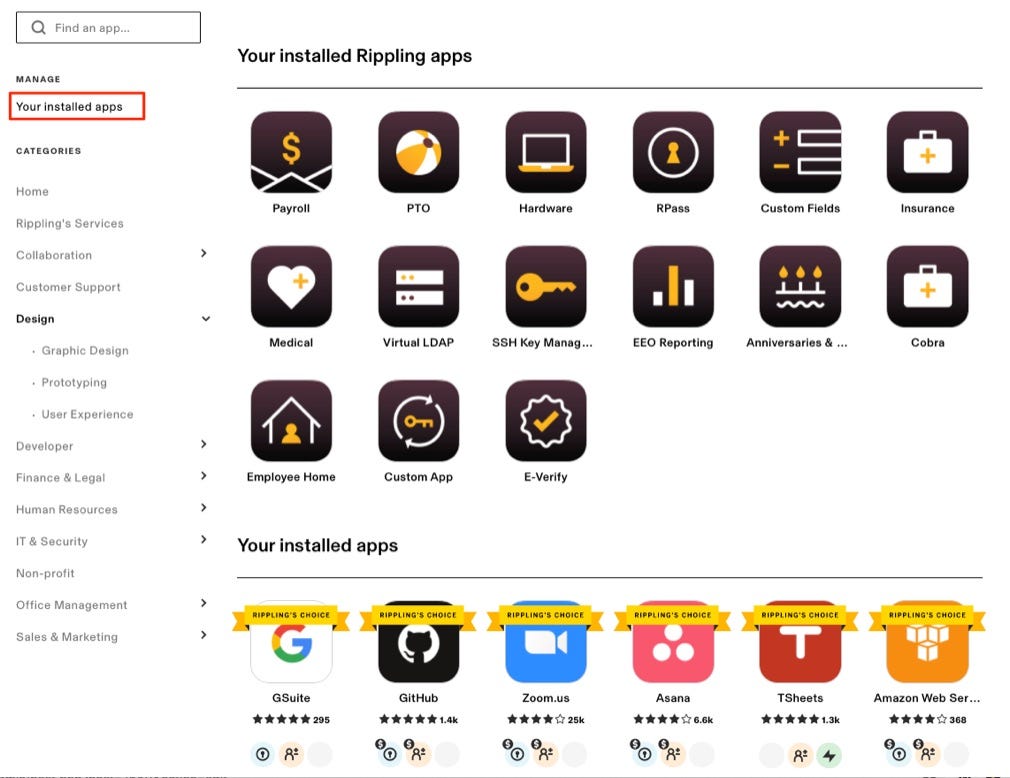

For non-founders out there, try to imagine hiring an employee. There’s payroll, benefits, Microsoft Office, Google Suite, other software they may need like Salesforce or Monday.com, legal resources, time tracking, and on and on and on.

While there is software for all those tasks, onboarding a new employee into all those entities is a separate and menial task that requires setting up many different accounts and wasting a lot of time during the onboarding process. Therefore, it’s still a file cabinet process in a way because it’s still very manual and slow.

Rippling essentially built an app-store-like platform to bring all of those separate software into one place where all information and data can be transferred among one another. Therefore, your new hire makes an account, and you assign them to whatever software they need access to, and they’re set up in no time. For a large company onboarding multiple people a day, this is a game-changer and saves so much time.

So that’s what Rippling was once they launched their product. But once again, Initilaized invested when this was just an idea. Actually, I suppose Coinbase and Instacart at least have very low-level MVPs; Rippling had nothing.

So, if you’ve read my essays before, something should be going off in your head that this was likely an investment based on the founder, which, I’d say, you’re right.

Garry Tan originally met Rippling founder and CEO Parker Conrad at Y Combinator when Parker went through the accelerator with his first company, Zenefits. Back then, and still to this day, Garry considers Parker one of the best founders he’s ever met. He is just an incredibly sharp guy who can emit such a clear vision and provide such a high-value product for a user.

The combination of improving the lives of users through software led by an incredible founder might make you think, “Huh, this sounds like an interesting place to work…” Well, if you’re feeling that way, then you know how the Initialized partners felt, especially Garry Tan when they made this investment. In fact, one of their investment theses is investing in companies they’d want to work for. Garry Tan described this principle as follows,

“It's like, "Hey, this person made a thing that's awesome. If they can make this, they're going to attract other people who can recognize that this is awesome. Through the like attracts like principle, this is going to be a magnet for all the other smartest people who know how to build."

I think that's underrated, actually. People don't realize this, but people who are really, really good at building really like working with other people who know how to build. That's the real currency of being able to build software in Silicon Valley is actually where the builders go, and where they want to work, that tends to be the thing that is the future.

We still use that as one of the primary things that we look for when we sit across the founder is if I weren't doing what I'm doing now. If I were going to go look for a job, would this be one of the top 10 places that I would want to go work at? Can you convince me? Then we look at all of each other with all of these different backgrounds. It's like, would all of us go work there? The cool thing is if you have a fund that is a bunch of people who, if you did go work there, you'd be a pretty good startup.”

There are two reasons why debating whether you’d want to work at that company is such a good filter for a startup investment. First, you kind of are going to be working there. If you invest in this company, you will be partners for a decade, and you will have to do whatever you can to help them, so you better get along with the founder and be aligned with the mission.

Second, as Tan emphasized, if the idea is really interesting to you and, ideally, other people you know, then chances are other exceptional builders will want to work at that company, which leads to even more builders wanting to work there, which eventually leads to a Golden-State Warriors-like super team essentially too talented to fail.

Since Tan admired Parker Conrad’s operating ability and aligned with Rippling’s mission of making all the annoying manual onboarding processes automated and simple through re-bundling all these unbundled SaaS products, he would’ve worked there, and therefore would assume other exceptional people would too because Garry Tan is quite the filter for an exceptional startup employee.

As a result, Initialed led a $7m seed round in Rippling, to which I’d assume they invested somewhere between $3.5-$4.5m in a crowded round. If that is the case, and Initialized is following their 10% ownership target, they likely have about $1.1 billion in value in their Rippling stock. I’m not sure how much they’ve invested in total, but I expect this will be at least a 100x investment for Initialized, and maybe even a $1 billion return, multiplying the total fund many times over.

Anti-Portfolio:

As I touched on in the intro, this is going to be less of our traditional investor-focused anti-portfolio section and more of a founder-mistakes-to-learn-from section. We will discuss three separate instances in Garry’s founder journey where he made crucial mistakes that were very avoidable had he known the lessons we’re about to discuss here.

Garry’s $350 million mistake:

In 2003, Garry had just graduated college and started his career as a Product Manager at Microsoft. He was one of probably thousands doing unexciting work, but coming from an unstable and poor upbringing, he thoroughly appreciated the consistent $72,000-a-year salary.

Shortly after he started at Microsoft, Peter Theil, co-founder of PayPal, was starting a company, Palantir, with some of Garry’s friends from school. They suggested that Peter meet with Garry to bring him on as a co-founder. So, Peter met with Garry and offered him $72,000 in cash, equal to his current salary, with a large ownership stake in Palantir and a slightly lower but nonetheless consistent yearly salary.

Essentially, it was a no-risk bet in most people’s eyes, but to Garry, he’d lose his safe job where he could slowly climb the corporate ladder and get more and more secure.

As Garry reflected on this moment, he realized he made a mistake for a few reasons. First, he didn’t understand equity vs. salary. A salary is something a company pays you out of the money they earn from your work, so while Microsoft was making hundreds of thousands of dollars, if not millions, in profit per employee, Garry was only making $72,000 of that. Whereas at Palantir, he would’ve directly owned the rewards of his contributions to the company at a fair value due to his ownership, which, as we know today, would’ve been worth about $350 million. Always favor equity over salary if you see potential in the company to grow because then you’re not creating value for users that other people benefit from; you’re creating value for users that you benefit from.

Second, he didn’t know who Peter Theil was. If you’re exceptionally skilled at some task, people will seek out your abilities. In 2003, Peter Theil was a big name in the startup community. He had recently sold PayPal, a company he co-founded, for about $1.5 billion. So, while Garry wasn’t versed in the startup community, he should’ve learned more about Peter before their meeting so he’d better understand how qualified this person was to get him to leave his job. Always prepare yourself for opportunities because you never know how valuable the outcomes can be.

Garry’s mistake when pitching Benchmark:

As regular readers/listeners know, Benchmark is one of the premier VC firms. This has been true since their founding almost 30 years ago, so it was especially true in 2010 when Garry Tan and his co-founders were raising their Series A for their company Posterous.

They were finishing up their pitch when Benchmark partner Peter Fenton asked, “So, are you a platform or a network?”

Unfortunately, Tan and his co-founders answered both, which was the wrong answer.

A general rule of thumb: if someone is asking you an either/or question, very rarely is both ever a good answer, but in the context of product positioning at a crucial stage of growth, answering both to this question is a really bad answer.

For context, A network is something that’s free for the users to contribute to create value. So, Instagram is a network because it relies on users coming to the platform to generate content to improve it for free. Instagram makes money from ads. Squarespace, on the other hand, is a platform that enables businesses to build websites on top of their software for a monthly fee.

So maybe you can see how it’s impossible to be both. If you’re both, then you’re not one or the other, and a company solely focused on being a platform or being a network, will beat you because they’re more focused on their core product positioning.

Unfortunately, Posterous could’ve been a platform or a network. Either would’ve worked for Posterous, as it was very similar to Squarespace. It was a blogging/website builder that let you share any of your posts on all social media platforms, which was fairly novel at the time. So they either could’ve dove deeper into pictures and become Instagram or started charging for users to build on their platform and become Squarespace.

It’s important to build things people want, which Posterous did as they had about 20 million users, but you also have to know how to steer the ship. You have to develop business strategy and know where you fit in the competitive landscape, or more focused competitors will wipe you out.

Clearly, Tan and his co-founders did not have a clear vision for the business based on their competitive landscape and how they could provide the most value for users while effectively capturing some for themselves. An investor won’t invest in a company that does not have that vision outlined because no matter how good the product is, a better-organized and well-positioned business will ultimately win.

Thus, Benchmark made the correct decision to pass on Posterous and invest in Instagram, and Tan and his team made the wrong decision of trying to be both a platform and a network.

Garry’s issues with his co-founder:

Issues with co-founders arise from either too much conflict or not enough conflict.

Founder drama happens even in situations where you wouldn’t expect it to crop up. For example, when things in the business are going up and to the right, you may be unaware of some underlying issues because you’re just watching revenue grow. Garry calls this the “black ice of startups” because every startup will hit skids sooner or later, but ones you didn’t see coming or ignored for so long while they built up have the most negative effects.

Posterous grew 10X yearly and became a top 200 Quantcast website in 2010. When things were going well, there were no major concerns to discuss. Why not just compromise in the argument with neither side going away happy? Growth will continue anyway. But by the end of 2010, growth had flatlined, and that’s when all the issues that were pushed aside surfaced in a big way.

Garry learned the hard way that if you haven’t prepared for conflict in your co-founder relationship, you’ll be at each other’s throats right at the moment when you most need to be working well together, which are the most challenging moment in a company’s history, not the most fruitful.

Garry and his cofounder's mistake was avoiding the dynamics of their co-founder's marriage altogether. They rarely spoke directly and honestly with one another and didn’t stop to reflect on what each other needed. They never sought professional support to ensure the health of the partnership, and when the honeymoon ended, there was no healthy foundation to support the company.

It’s funny because that last paragraph really does sound like a marriage, but that’s why so many co-founders compare these relationships to a marriage. Co-founders must be completely honest with one another and provide a platform for disagreements and debates to arrive at the best outcome. Though it may not feel like it at the time, typically, a compromise is the worst thing you can do because both sides didn’t get what they wanted, and not even debate occurred to arrive at the ideal solution for the business regardless of the co-founder’s feelings.

At the end of the day, it’s not about the co-founders’ feelings, it’s about the customers you’re serving and the employees on your payroll.

If you want to 2x spend on growth and your co-founder wants to 4x spend on growth, then if you compromise and settle on 3x spend on growth, no one is happy. You think you’re growing too fast, and your co-founder thinks you’re going too slow. Though the compromise seems even, it’s actually a lose-lose.

Be honest and embrace disagreements. The more water under the bridge, the greater the flood once the cracks begin to show.

To sum up, founders: recognize the importance of long-term equity over short-term salary, prepare yourselves for exceptional opportunities when they present themselves, have a clear vision and position your startup accordingly, and have an honest relationship with your co-founders.

While Garry made these mistakes early in his career, I don’t think he’s too upset about it. Sure, he missed $350 million in Palantir, and who knows how much if Posterous succeeded, but he has personally made likely over $1 billion on his 27 unicorn investments with Initialized Capital, so it’s safe to say he doesn’t regret the outcomes of his mistakes.

After all, failure is just the tuition you pay for success.

Conclusion:

If you’re not in awe of how exceptional Initialized’s 12-year run has been since its founding after reading this post, then I didn’t do a great job because they are certainly one of the most successful firms we’ll ever investigate. As I said, 27 unicorns in 12 years. Many top VC firms hope to hit one unicorn a year; Initialized is averaging nearly 2.5 a year.

While Tan is back at YC, the foundational investment theses of the firm will remain, and they will likely continue to be one of the best unicorn hunters in the world.

That is all for today; if you liked this essay, please share it with a few friends you think would be interested! I’m sure they’d be grateful you sent it to them. Also, if you want to listen to the podcast episode, you can do that here: Spotify - Apple. If you want to watch clips from the podcast episode you can check out the YouTube page. If you want to learn more about the companies a16z invested in that we didn’t cover and more investment theses of the firm and tips for founders, you can check out allthingsvc.blog. Lastly, you can follow me on Twitter, @Justin_Pryor_ for random tweets regarding the companies I cover and the lessons I learn.

Thanks again for reading! Stay tuned next week for another insightful essay.