Loyal: Your Best Friend's (and Investor's?) Favorite Company

Loyal: Your Best Friend's (and Investor's?) Favorite Company

Plus, How VCs Analyze a High-Technical Risk, Low-Market Risk Startup Through Scenario Analyses

Intro:

Something I really appreciate about humanity is our openness to a good debate. We often see this in business. For example, in my last post, some could say Wal-Mart’s cheapest pricing strategy prevented mom-and-pop general stores from being able to compete and wiped out many small businesses. On the other hand, I would say the cheapest prices model benefitted consumers most, which a free market optimizes for. As a result, more specialty mom-and-pop stores arose to counter-position themselves and compete, which also benefitted consumers. My point is that these claims can be argued.

Loyal is perhaps the first company where I refuse to hear any argument that isn’t regarding how great this company is for the world.

Loyal is developing a safe and non-abusive longevity drug for dogs that will extend their lives by another year or two. How can you not root for this company?! That’s an incredible mission that everyone can get behind.

The largest dog breeds typically only live 8-10 years, medium 10-12, and smaller dogs a little longer. Dog owners know these pets can feel like family members, so how short their lives are is awful.

I’m also going to spare any of the biological details of how this all works, but recently, Loyal received conditional approval from the FDA, meaning they can begin selling medium-sided dogs in 2025 and large and giant breed dogs in 2026. They have three different drugs for each type of dog in this group.

Conditional approval means Loyal can sell these drugs, but a veterinarian cannot prescribe them, and they cannot claim they are FDA-approved. Conditional approval means these drugs likely do as Loyal claims, but they need a few years of data to ensure they absolutely do as Loyal claims. This process could take anywhere from 2 to 5 years since they have to prove it elongates dogs' lifespans, which obviously takes years and many dogs to ensure.

So Loyal is in an interesting period where they can sell the drugs to consumers directly, but it’s not covered by insurance, probably much more expensive than they’ll eventually charge, and it’s not guaranteed to make your dog live longer. Therefore, during this conditionally approved stage, they likely won’t sell a lot of drugs, probably only to the most die-hard dog lovers, though perhaps enough to be breakeven or somewhat profitable. Also, they likely won’t have any serious competition until they’re FDA-approved, so technically, they currently have a monopoly on the dog longevity drug market. It’s a weak monopoly but a monopoly.

The three big questions facing Loyal now and in the future in investors minds are:

How much of their drug can they sell while in the conditionally approved stage?

Will they be FDA-approved? If not, the company may die or lose to a competitor.

If they are FDA-approved, how long will their monopoly continue?

All of these questions are extremely speculative for an outsider like me and, basically, anyone without direct connections to the company because no one outside the company knows how complex their drug is.

What I think is more interesting at the moment, or at least what I can write about, is how a seed-stage investor may have analyzed this company. After all, if Loyal successfully proves they can increase the lifespan of dogs, they will have a short-term monopoly on that market and likely generate significant cash flow. On the other hand, there were many places where their research could’ve failed, and Loyal could’ve gone out of business.

Therefore, this essay will include several scenario analyses that a seed-stage investor may have built when considering investing in Loyal back when it was just an idea.

This blog post is going to have A LOT of spreadsheets showing you how a VC would calculate the risk and reward in these highly technical investments where the technical risk is high, but the market risk is basically negligible. As you’ll see, Loyal will likely be a multi-billion dollar company if its drug gets FDA-approved.

Before going into the spreadsheets, I’ll elaborate on key inputs like the market size, the potential CAC-LTV for Loyal, and the chances of this drug getting FDA-approved. These are the key levers when considering Loyal for an investment, and it is an exercise I suspect many deep-tech investors conduct. These three levers drastically change the company's valuation, so we’ll analyze many different scenarios regarding the low-end to high-end of certain projections.

The Market:

Price: $40-$50 a month. The Loyal CEO said in an interview that it would be $30-$70 a month, so I’m assuming they price it in the low-medium of that range.

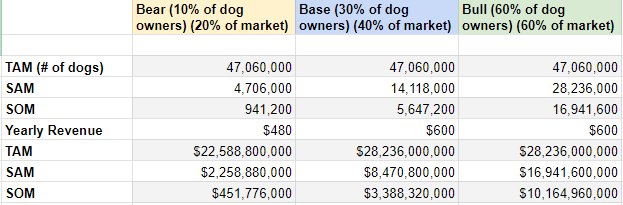

TAM:

62 million U.S households own an average of 1.46 dogs, so there are about 90.5 million dogs in the U.S. 52.4% of households have a dog 7+ years old

Since Loyal is targeting dogs 7+ years old, their TAM is 90.5m dogs * 52.4% = 47m dogs.

SAM/SOM:

Bear:

In this scenario, while the data shows dog owners say they care about their dogs tremendously, most don’t care enough to pay $40 a month for an extra year of life. Only 10% of dog owners adopt the product. Also, competitors quickly arose without much discrepancy, maybe offering a cheaper alternative, meaning Loyal only held 20% of the dog longevity market.

Base:

In this scenario, the percentage of dog owners that pay for Loyal is closer to the data but lower than the data would suggest. Maybe only two or three viable competitors enter the market, giving Loyal a 40% share due to their first-mover advantage.

Bull:

In this scenario, slightly more dog owners than expected use Loyal, and Loyal maintains a strong market position as only one or two viable competitors enter the market.

Overall Thoughts on the Market:

Once again, these are all based on assumptions, but it’s a good exercise to work through. Normally, the founder of Loyal would do this exercise and tell an investor what they think their market is based on the research they did. The articles I used are good, but the Loyal team likely did more extensive research than my few hours. An investor would then trust but verify this information and give their own opinions on the bear, base, and bull case scenarios.

If I had to guess, I think Loyal will be sold to ~50% of dog owners based on the data I found on how many dog owners love their dogs like true family members and can afford something like this. Also, I think they will command 50-60% of the market. This is a revolutionary drug—the first of its kind. Therefore, I’m basing its market share on Novo Nordisk’s market share in the weight loss category for its Wegovy and Ozempic products. Novo Nordisk controls 55% of that market, while Eli Lilly is the only other strong competitor. I suspect Loyal will see similar results based on how big a breakthrough this product is, but I’m sure a few viable competitors will quickly enter the field. However, the first-mover advantage here will be apparent.

Why so apparent? Dog owners who are willing to pay $480 a year for their dog to live an extra year will immediately pounce on Loyal’s drugs once they're available to the public and FDA-approved. Therefore, this cohort will start their dog on Loyal before any other viable competitors can enter the market. That target market will already be committed to using Loyal for the next several years of their dog's life, as I’m sure you can’t switch while using these drugs, even if they’re fairly similar. Therefore, a competitor will have to wait for the next wave of dog owners with dogs 7+ years old, with which Loyal will still actively compete. Holy first-mover advantage!

I suspect Loyal takes 100% of the SOM as soon as the product is released, keeps that SOM due to expected switching costs, and then it becomes maybe a 50/50 battle with another competitor or two as new dog owners enter that SOM. However, Loyal will already have such a massive market share from those first adopters.

I’d also like to note that most bear cases for startups are not $450 million in revenue. That is obviously a fantastic outcome for any startup. Loyal, however, is creating the first-ever dog-longevity drug, so, as I said, the market risk is nearly negligible. It’s just a matter of how many dog owners love their dogs enough to pay ~$500-$600 a year for them to live another year or two.

A general software company may have a bear case in the double-digit millions range to show that they’re still a viable M&A candidate if they don't break out due to market competition. Loyal’s bear case is still wildly successful, thus making the technical risk such an important factor in this investment decision, which we’ll get to later.

LTV:CAC:

LTV:CAC is nearly impossible to estimate without proprietary information and a product even in the market. However, I can at least estimate the LTV based on certain price points for the product and its effectiveness.

Bear:

Loyal charges $40 a month for their product with an 80% gross margin—the low end for successful pharmaceutical companies. Their drug only adds 6-12 months extra life for dogs, making the lifetime use of the product three years, and they have a pharma-industry average LTV:CAC ratio.

Base:

Loyal charges $50 a month for their product with an 85% gross margin—average for successful pharma companies. Their drug extends a dog’s life for a full, year giving them a 4-year lifetime use of the product along with an above-industry average LTV:CAC ratio.

Bull:

Loyal charges $50 a month for its product, which has a high 87.5% margin, while delivering two full years of life extension for dogs using the product for five years. The product also has an exceptional CAC:LTV ratio.

As I mentioned, typically, a company calculates its CAC and then estimates its LTV. However, for Loyal, we know more about the LTV rather than the CAC. This ratio isn’t too important for Loyal because their drug is so revolutionary that it should sell easily. If one dog owner sees an ad, they will tell all of their friends because they will be so amazed this product exists. Word-of-mouth marketing will likely be incredible for this product.

Loyal has very strong potential customer LTV, depending on how effective their drug is. It’s also very predictable since customers likely won’t churn until their dog passes away, or else the effects will likely wear off, and they spent all of that money for nothing. There are no revenue expansion opportunities like in other SaaS companies that charge per seat since it’s one drug for one dog. Still, as the chart shows, their LTV will likely be at a minimum of three years with very low churn, which is quite remarkable for any subscription business.

A Note for B2B and B2C SaaS Founders Regarding CAC:LTV:

SaaS businesses should generally focus on their customer payback period in the early stages before they have definitive data on how long their customers stay on their product. If you’ve only been in operations for a year but predict your customers will stay for five years, you can fall into the trap of paying three years of customer revenue to acquire them since you believe you’ll have them for five.

You have no idea if this is the case just a year in because a better SaaS product can be released any day. Therefore, for businesses with lower technical risk like B2B or B2C SaaS, a founder should focus more on the CAC Payback Period, which works backward from CAC to say how many months or years you need a customer to pay for your product to break even.

You typically want to be below twelve months, with the best SaaS businesses in the 5-7 month range.

I suggest ignoring CAC:LTV in the early days until you have more definitive information about how long your customers will stay rather than predict. Then, you can spend more on CAC if you’re confident about the length of your LTV, but in the early days, try to keep that payback period below twelve months, or else investors will think customers don’t love your product and your growth is fueled by ad spend rather than product-led growth.

Again, one caveat is a low-market-risk company like Loyal, where you can reasonably predict how long a customer will use the product due to lock-in, that’s when you can use CAC:LTV early on.

Is this Investment a No-Brainer? Scenario Analysis:

Perhaps my typical extreme optimism is giving you the impression that this is a no-brainer investment and every investor who passed is stupid. Maybe I agree with you, maybe I don’t, but what I’m going to do now is put in images of a bunch of spreadsheets to show how a seed investor may have analyzed this investment based on the technical and market risk.

You already saw the market risk chart above for the bear, base, and bull case, but let me elaborate on the numbers I chose to describe the technical risk.

Since this drug is completely revolutionary, I assume the technical risk is quite high. Therefore, I assigned the values 2.5%, 5%, and 10% for the bear, base, and bull cases, respectively. It seems like most VC-backed startups have a 10% chance of an IPO or large acquisition, so I put a bit of a handicap on that for the technical challenge ahead of the Loyal team, or at least, how an investor may have viewed it.

(I made a YouTube video going through each analysis, which may be a little more entertaining. If you’d like to check that out, CLICK HERE)

In case you’re too lazy to scroll up, here are the market risk scenarios once again:

As a reminder, before I go into these assumptions, this is solely based on my research. I have no idea if investors who considered the deal had similar numbers to me, but I think I’m at least in the ballpark.

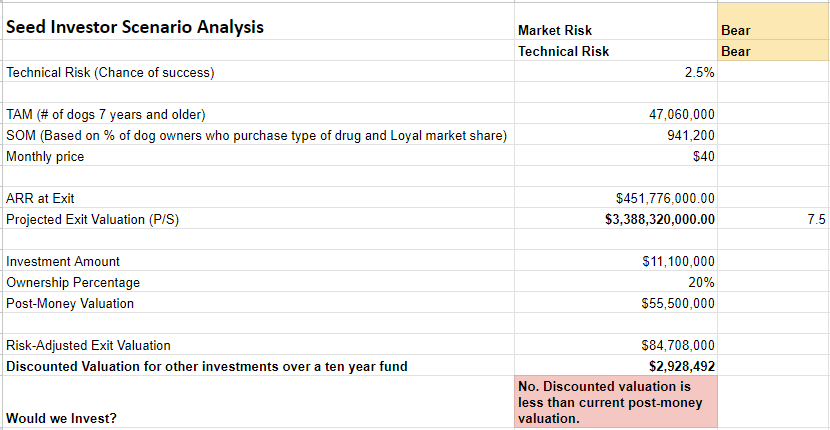

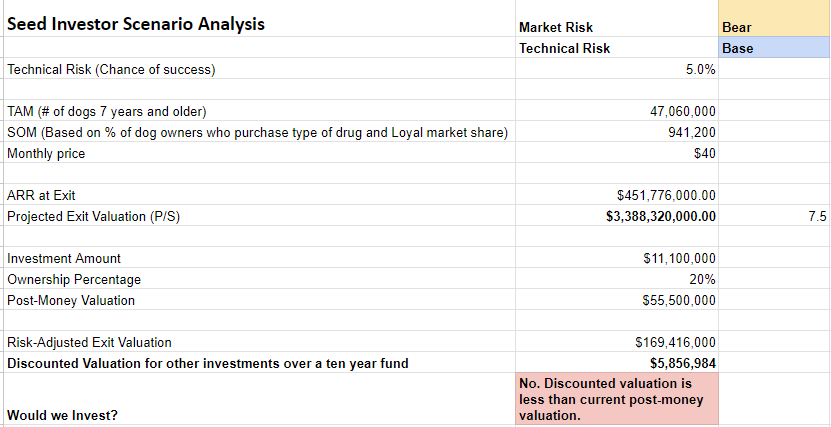

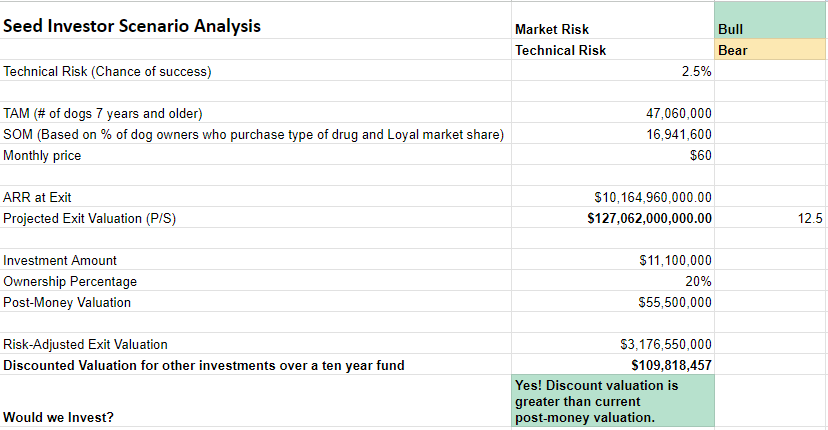

Technical: Bear (2.5%)

Market: Bear (SOM: 941,200)

So I’m going to explain this one line-by-line, and then you’ll be able to interpret the rest of the charts without my explanation.

ARR at Exit: SOM multiplied by the monthly price multiplied by 12.

Projected Exit Valuation: I used the price-to-sales ratio of 7.5 here. Novo Nordisk, the gold standard right now for pharma companies, is around 15 price-to-sales, so in my bear case for the market, Loyal is valued slightly less than that due to higher competition and lower SOM than Novo Nordisk. As you’ll see, the base case is 10, and the bull case is 12.5. It's not quite Novo Nordisk level since Novo has a much larger market.

Investment Amount: The actual seed round for Loyal was a $11.1 million raise. I don’t know how much equity she sold, however, so I’m just going to go with the general 20%, which values the company at $55.5 million.

Risk-Adjusted Valuation: This is if you just took the projected exit valuation based on the market outcomes in the bear scenario and multiplied it by 2.5% (the technical risk).

Discounted Valuation: Since an investment in Loyal means one less investment in another startup, we have to calculate some opportunity cost for investing in Loyal and not another startup with 40% IRR potential (the target return for a top decile VC seed fund). The equation I used was 84,708,000 / (1+0.4)^10.

Would we Invest? No. The discounted valuation is $2,928,492, while the valuation at this seed investment is $55,500,000. Since the discounted valuation is (much) less than the seed investment valuation, we would not invest if we were bearish on technical and market risk.

Do I know this is how VCs calculate a risk-adjusted present value? No. In fact, from what I’ve seen, it seems like most seed investors don’t even do this much financial analysis. Since we’re just learning here though, I thought it would be interesting.

Now, for the rest of the scenarios, there will be different market and technical risks, and you’ll see when an investor would invest and wouldn’t.

Technical: Base (5%)

Market: Bear (SOM: 941,200)

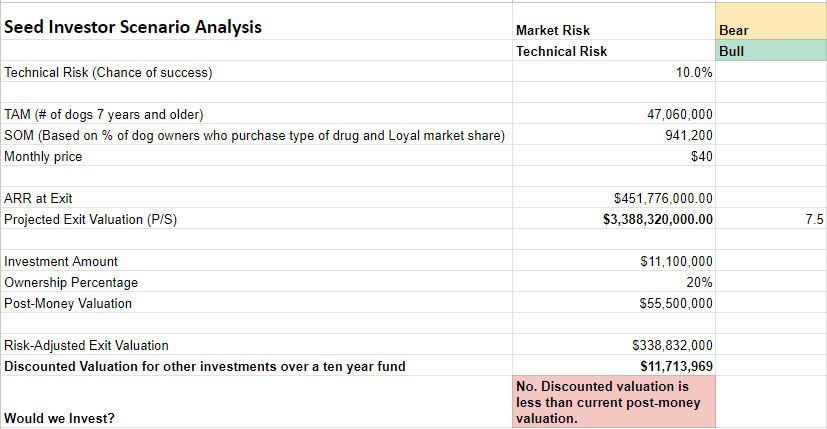

Technical: Bull (10%)

Market: Bear (SOM: 941,200)

Technical: Bear (2.5%)

Market: Base (SOM: 5,647,200)

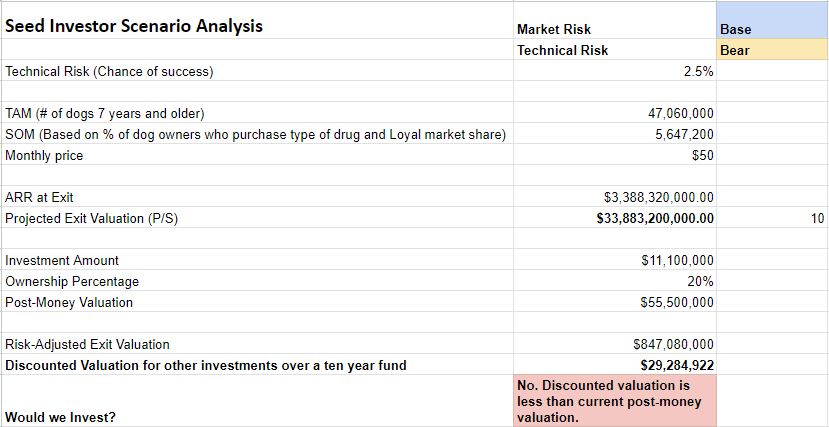

Technical: Base (5%)

Market: Base (SOM: 5,647,200)

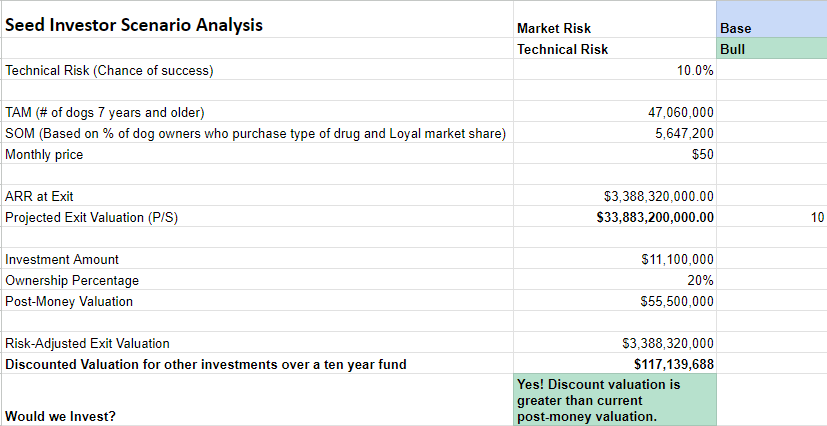

Technical: Bull (10%)

Market: Base (SOM: 5,647,200)

Technical: Bear (2.5%)

Market: Bull (SOM: 16,941,000)

Technical: Base (5%)

Market: Bull (SOM: 16,941,000)

Technical: Bull (10%)

Market: Bull (SOM: 16,941,000)

Debrief:

So, based on my assumptions, I’d invest in 5/9 of these scenarios for Loyal. You can interpret that as I have a 55% chance of a positive outcome, or you can interpret that as I have a 55% chance of an outsized return, much greater than 1x. In the scenarios where I wouldn’t invest, I only lost my $11m, whereas I could make over $6 billion after dilution in my most bullish example (which maybe is too bullish…)

Based on these analyses, I would certainly invest in Loyal. I’m not an expert on drug development, and some VCs may have given it a 1% chance of success, while others may have given it 20%. What I do feel confident in is that if the drug is successful, Loyal hits either my base or bull case market outcomes.

Interestingly, during Celine’s (the Founder and CEO) fundraising for Loyal’s seed round, only 17/157 investors wanted to invest. I’m extremely curious to know why those investors who said yes did, but even more curious to know why some said no, what they thought about Loyal, and what analyses they did.

Did they not predict as large a market as I did? I actually don’t think I was super bullish, especially in my bear and base case. Did they think the technical risk was something like 1% or 0.5%? Is it just not an industry they invest in? After all, VCs are somewhat constrained by the industries they tell their LPs they’re going to invest in. If a B2B SaaS-focused VC firm invests in biotech and it fails, their LPs will consider them undisciplined and may not invest in their next fund.

Yes, This is Deep-Tech, But There are Levels:

I want to finish by saying this isn’t a bull case for deep-tech. While I am personally more interested in startups that can own a market, ideally one they build themselves, I don’t think every deep-tech company commands their market as much as Loyal might in the future.

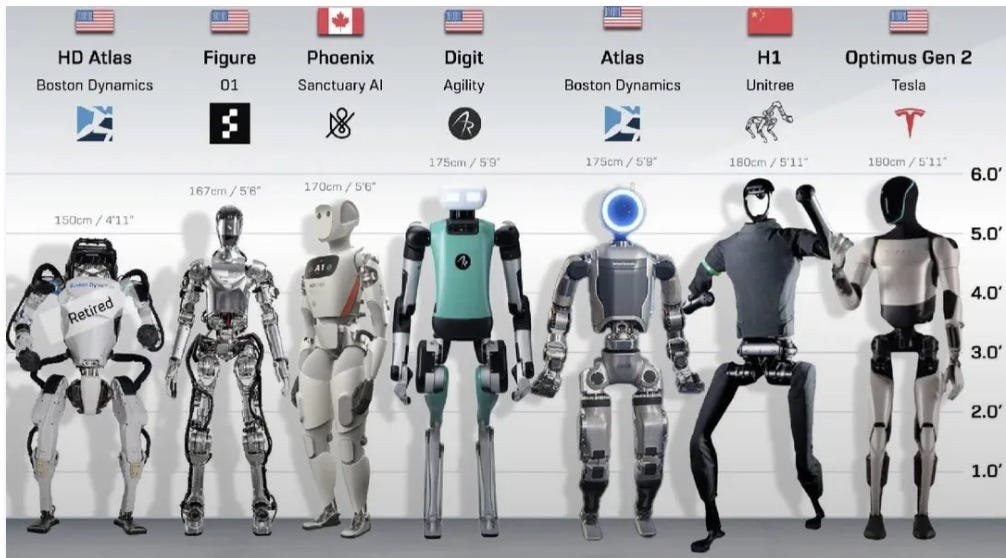

Take FigureAI, for example. They’re one of the hottest deep-tech companies out there because they seem to be the leader in humanoid robots. But, just because they’re the leader doesn’t mean they’ll capture the market.

As you can see, FigureAI already has some major competitors, even though we’re very much in the first inning in AI-powered humanoid robots, so that isn’t necessarily an industry I’d want to play in. FigureAI seems incredibly fascinating, and I’d certainly look into investing if I could, but I see this industry more as specialist robots rather than general all-purpose robots—a robot specialized in building bridges, or buildings, or working on oil rigs, and so on. Perhaps these humanoids work well in distribution centers as copy-for-copy human replacements, but eventually, those would get replaced with something faster that’s built for distribution centers only.

If I were investing in this space, I’d lean towards investing in the absolute best bridge building/bridge repair robots in the world because that can be a multi-billion dollar market that they can lead with first-mover advantages and likely expand since everyone wants to repair bridges, people just don’t want to pay the cost nor have the necessary human labor resources. If there are robots you can just cheaply rent and deploy for a few weeks to get the job done, then more governments will pay more frequently for that service, leading to market expansion. (More on this next week, perhaps…)

The point is that just because something is deep-tech or hard-tech, it doesn’t mean the market risk is zero. Even a software company can create something with no market risk. After all, Microsoft Excel has been THE de-facto spreadsheet software for almost forty years now!

So, this post isn’t an overall endorsement for deep-tech companies. Maybe it’s an endorsement for biotech, which I’ve never really looked into before. It’s mostly an endorsement for the old-school startups creating something revolutionary that builds an entirely new market for consumers.

Humanity has built so many incredible things in the last 50 years that it can seem like many of these problems have been solved, but they haven’t; they’re just getting harder. There are always some brave builders like Celine Halioua out there who are building something that’s one of a kind and creates its own market. Bonus points for saving dogs' lives!

(Reminder: Check out the YouTube page for the scenario analysis explanation video, along with many other videos and clips from this post and previous ones.